Self-Directed IRA Real Estate Pros & Cons : Lending vs Owning

Professional Photography: Carography Studios

A Professional Guide for Passive Retirement Investors Seeking Control, Compliance, and Predictable Returns.

Why This Decision Matters for Passive Self-Directed IRA Investors.

Self-Directed IRAs (SDIRAs) give retirement investors the ability to move beyond traditional Wall Street assets and deploy capital into real estate-secured opportunities. For passive investors in particular, this flexibility presents an important decision that can materially impact risk exposure, compliance burden, liquidity, and long-term retirement outcomes.

Two of the most common real estate strategies inside an SDIRA are direct property ownership and real estate-secured lending. While both are permitted under IRS rules, they differ dramatically in execution, oversight requirements, and suitability for passive retirement capital.

For investors seeking predictable income, reduced regulatory risk, and a hands-off structure aligned with long-term capital preservation, lending through an SDIRA is often the more practical and defensible approach. When implemented through a professionally managed structure, SDIRA lending allows investors to become the bank without assuming the operational and compliance responsibilities that accompany property ownership.

This article provides a compliance-first comparison of SDIRA lending versus ownership, with a specific focus on why professionally structured lending solutions, such as those offered through Blue Bay Fund, may be better aligned with the goals of passive SDIRA investors.

An alternative investment fund manager shaped by military rigor and entrusted stewardship.

MORE ABOUT EDWIN

Edwin D. Epperson III is the Fund Manager of Blue Bay Fund I, a real-asset investment firm focused on conservative capital preservation and income-oriented strategies. A former U.S. Army Green Beret, he brings a disciplined risk-management mindset to asset-backed investing and portfolio construction for accredited investors.

About Blue Bay Fund I

Blue Bay Fund I focuses on asset-backed real estate strategies designed for investors prioritizing capital protection, structured income, and long-term stewardship. The firm emphasizes disciplined underwriting, regulatory awareness, and conservative portfolio construction.

Understanding Self-Directed IRAs and Real Estate Investing

Self-Directed IRAs for Real Asset Investing

Gain greater control of your retirement capital while investing with structure and protection.

A Self-Directed IRA is a tax-advantaged retirement account that allows investments in alternative assets beyond publicly traded securities. These assets may include real estate, private mortgage lending, notes, precious metals, and private equity.

Unlike traditional IRAs, SDIRAs place investment decision-making authority with the account holder, while a qualified custodian administers the account and ensures IRS reporting and procedural compliance.

This structure offers flexibility but leaves little room for error. IRS rules governing SDIRAs are strict, and violations can result in immediate account disqualification and taxation of the entire account value. Having a custodian reviewing investment decisions for legal compliance, and investing through a fund manager, focused on risk mitigation, such as Blue Bay Fund, help to negate most, if not all, potential violations.

SDIRA vs Traditional IRAs: Structural Differences

Traditional vs. Self-Directed IRAs: Expanded Control, Elevated Responsibility

Traditional IRAs are generally limited to stocks, bonds, ETFs, and mutual funds. Self-Directed IRAs expand the opportunity set but require deeper regulatory awareness and investor discipline.

Key differences include broader investment options, increased administrative complexity, higher compliance risk, and greater responsibility placed on the investor.

Because SDIRAs often hold illiquid assets, careful planning and conservative execution are critical to long-term success.

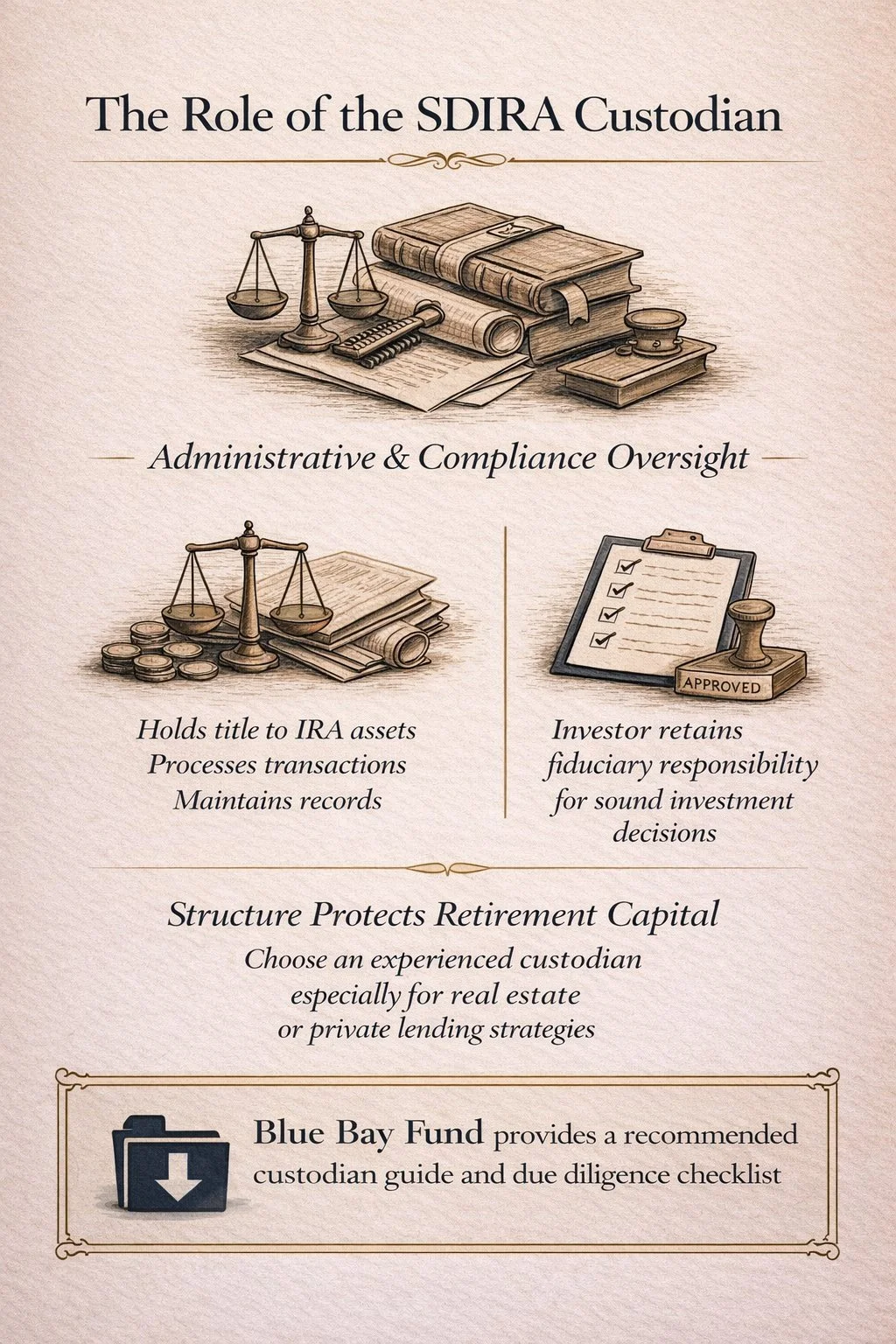

The Role of the SDIRA Custodian

Structure Before Strategy.

An SDIRA custodian does not provide investment advice. Their role is administrative and compliance-focused. Custodians hold title to IRA assets, process transactions, maintain records, and report required information to the IRS.

Custodians review transactions to identify potential prohibited transactions, but the fiduciary responsibility for wise and sound investment decisions remains with the investor. Choosing an experienced custodian is essential, especially when investing in real estate or private lending.

Blue Bay Fund has provided a download with recommended custodians and questions you should ask potential SDIA custodians in helping you make an informed decision on who to host your SDIRA with.

Lending Through a Self-Directed IRA

Photography: Carography Studios

How SDIRA Lending Works

In an SDIRA lending strategy, the retirement account itself serves as the lender rather than the individual account holder. Capital is deployed into real estate-secured loans, and the SDIRA is listed as the lender on all loan documents. Borrower payments, including principal and interest, flow directly back into the retirement account.

Unlike direct ownership, lending does not require the investor to manage tenants, oversee property operations, or make ongoing execution decisions. However, one of the largest drawbacks to lending through an SDIRA is that the investor must have 100% of the loan request in liquid, unused funds. This reality can create return-drag, pulling the overall performance of the SDIRA down.

For many passive investors, lending is most effective when accessed through a professionally managed structure rather than sourcing, underwriting, and administering individual loans independently. Blue Bay Fund provides a centralized platform that allows SDIRA investors to participate in real estate-secured lending while maintaining proper documentation, disciplined underwriting standards, and operational consistency.

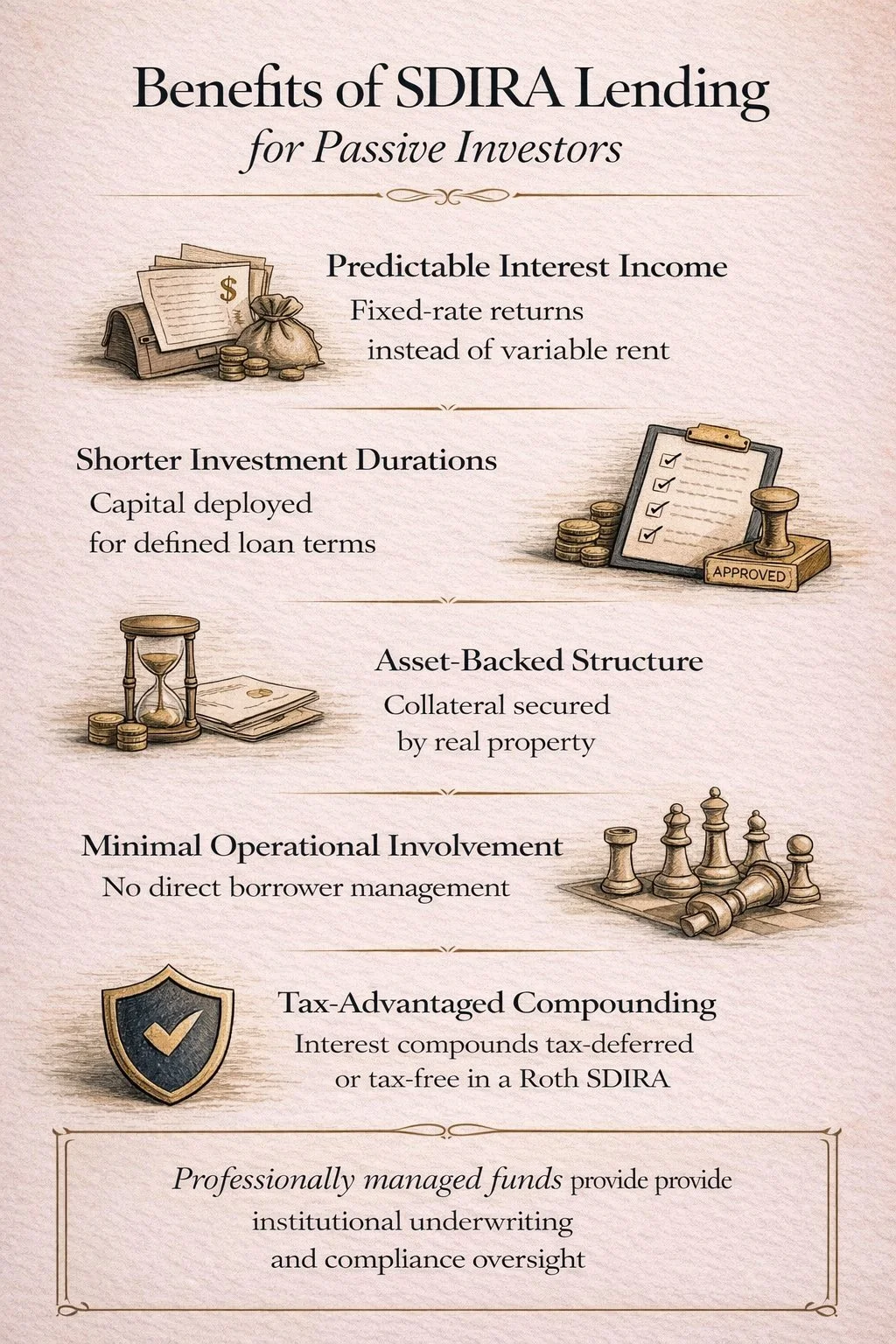

Benefits of SDIRA Lending for Passive Investors.

When structured conservatively and professionally, SDIRA lending offers several advantages that are particularly relevant to passive retirement investors:

Predictable interest-based income rather than variable rental cash flow

Shorter investment durations compared to long-term property ownership

Asset-backed collateral with defined loan terms

Minimal operational involvement and decision-making

Reduced exposure to accidental prohibited transactions

Interest income earned through SDIRA lending compounds on a tax-deferred basis, or tax-free in a Roth SDIRA. By investing through a professionally managed fund, SDIRA investors benefit from institutional-grade underwriting and compliance oversight without taking on the responsibility of direct borrower management.

Risk and Compliance Considerations

Like all SDIRA strategies, lending requires disciplined execution. Risks include borrower default, collateral valuation errors, and improper loan documentation. Poorly structured lending activity may also introduce Unrelated Business Taxable Income (UBTI) concerns if it is deemed an active trade or business.

Professional oversight is a key risk mitigant. Blue Bay Fund emphasizes conservative loan structures, asset-backed security, and regulatory awareness, helping SDIRA investors participate in lending while maintaining a passive posture and strong compliance discipline.

Direct Real Estate Ownership in a Self-Directed IRA

How Ownership Works

When an SDIRA owns real estate, the IRA purchases the property, pays all expenses, and receives all income. The account holder may not live in, use, manage, repair, or personally benefit from the property.

All property-related expenses must be paid directly from the IRA, and all income must flow back into the IRA.

Advantages of Ownership

Long-term appreciation potential

Rental income growth over time

Inflation hedging characteristics

Direct participation in asset upside

These benefits can be meaningful over extended holding periods when managed carefully and compliantly.

Drawbacks and Compliance Risks

Direct ownership carries increased regulatory exposure. Prohibited transactions can occur easily if rules are misunderstood or inadvertently violated. Debt-financed properties may trigger Unrelated Debt-Financed Income (UDFI), creating tax liability inside an otherwise tax-advantaged account. SDIRA investor may also find it burdensome to identify and qualify for loans for the SDIRA account through traditional financing.

Ownership also introduces operational complexity, illiquidity, and higher administrative friction, which can be challenging for passive retirement investors.

Why Blue Bay Fund I Is Different

Lending vs Owning: A Strategic Perspective for Passive SDIRA Investors

While both lending and ownership are permitted within a Self-Directed IRA, they are not equally suited to passive investors. Direct real estate ownership requires ongoing decision-making, strict expense handling, and heightened awareness of prohibited transaction rules. Even well-intentioned investors can unintentionally trigger compliance violations due to the hands-on nature of ownership. Most financial institutions that offer loans to SDIRA’s to own real estate may require 50% or more down for property purchases.

Lending, by contrast, aligns more naturally with a passive retirement mandate. Cash flow is structured, responsibilities are limited, and the likelihood of accidental self-dealing is reduced. When executed through a professionally managed vehicle, lending allows SDIRA investors to fractionally participate in real estate-secured returns without assuming the operational or regulatory burden of property ownership.

For passive investors prioritizing simplicity, safety, and professional execution, structured SDIRA lending often represents the more prudent and scalable approach. By leveraging an experienced manager such as Blue Bay Fund, investors can access real estate-secured lending opportunities while maintaining clarity, compliance, and long-term retirement focus.

IRS Compliance and Prohibited Transaction Rules

The IRS prohibits self-dealing in SDIRAs. Disqualified persons include the account holder, spouse, parents, children, grandchildren, and entities under their control.

Common prohibited transactions include:

Personal use of IRA-owned property

Selling personal property to the IRA

Paying IRA expenses personally

Performing repairs or management services

Receiving compensation related to IRA assets

Violations can result in full IRA disqualification and immediate taxation.

Due Diligence Requirements

Due diligence is mandatory for both lending and ownership strategies.

For lending, this includes borrower analysis, collateral valuation, title review, and legal documentation.

For ownership, due diligence involves property inspections, market analysis, expense forecasting, management planning, and exit strategy evaluation.

Risk Management and Diversification

Effective SDIRA portfolios avoid overconcentration. Diversification across asset types, geographic regions, and deal structures helps mitigate downside risk.

Combining structured lending strategies with limited ownership exposure may provide balance while maintaining compliance discipline.

SDIRA investors, choosing to invest through a professionally managed debt fund, such as Blue Bay Fund are able to benefit from our strict underwriting and streamlined approach while also being able to participate with a fraction of the total loan amount instead of 100% of the loan. This introduces diversification, which is not available when SDIRA investors lend directly to borrowers.

Key Takeaways

SDIRAs offer control but demand discipline

Lending strategies generally carry lower compliance risk for passive investors

Ownership offers upside with increased complexity

Custodians enforce process, not investment quality

Prohibited transactions carry severe penalties

Professional guidance is strongly recommended

Frequently Asked Questions (FAQ)

Is real estate allowed inside a Self-Directed IRA? Yes. IRS regulations allow Self-Directed IRAs to invest in real estate, including rental properties, raw land, and real estate-backed lending, provided all transactions comply with prohibited transaction rules and are administered through a qualified custodian.

What is the biggest compliance risk with SDIRA real estate? The greatest risk is engaging in a prohibited transaction. This includes personal use of IRA-owned property, self-dealing with disqualified persons, or performing services on the property yourself. Violations can disqualify the entire IRA.

Is lending through an SDIRA safer than owning property? From a compliance and operational standpoint, lending is generally considered lower risk for passive investors. Lending involves fewer ongoing decisions and reduces the likelihood of accidental prohibited transactions.

Can I use leverage inside my SDIRA? Yes, but only non-recourse financing is permitted. Debt-financed property may trigger Unrelated Debt-Financed Income, which can create tax liability.

Who pays expenses for IRA-owned real estate? All expenses must be paid directly from the IRA. The account holder may not pay expenses personally or reimburse themselves later.

Do I need professional guidance for SDIRA investing? Yes. SDIRAs operate under strict IRS rules, and mistakes can be costly. Investors should work with experienced custodians, tax professionals, and managers who specialize in alternative assets.

Edwin D. Epperson III,

Manager & CEO

Soli Deo Gloria