Investment Due Diligence: A Complete Guide for Accredited Investors

The strategies, frameworks, and checklists that experienced investors use to evaluate real estate-secure opportunities organized by investor profile.

Whether you are a pre-retiree seeking reliable monthly income, a busy professional who wants truly passive real estate exposure, or a sophisticated allocator who demands deal-level transparency, rigorous investment due diligence is the discipline that separates confident capital deployment from costly mistakes.

This guide walks you through the strategies, frameworks, and evaluation criteria that experienced investors use to assess real estate-backed opportunities. You will find actionable guidance for every experience level, from foundational concepts to advanced risk assessment methodologies, all oriented toward the same outcome: protecting capital and generating sustainable returns.

What Is Investment Due Diligence and Why Does It Matter?

Investment due diligence is a structured, evidence-based process that evaluates an investment's viability, risks, and alignment with your financial objectives before capital is committed. It replaces guesswork with systematic analysis: verifying collateral, scrutinizing track records, stress-testing assumptions, and establishing monitoring protocols that continue long after the initial commitment.

For accredited investors, due diligence is not optional. It is the mechanism by which you distinguish well-managed funds from poorly structured ones, realistic return projections from marketing-driven ones, and genuine capital preservation strategies from superficial reassurances. A disciplined process protects your principal, reduces surprises, and significantly improves the probability of achieving your target returns across varying market conditions.

The form that due diligence takes should match who you are as an investor. A pre-retiree prioritizing monthly income needs to scrutinize collateral quality, distribution sustainability, and principal protection mechanisms. A busy professional with limited time needs a framework that delivers rigorous answers efficiently, without demanding weeks of research. A sophisticated allocator building a diversified alternatives portfolio needs deal-level transparency: loan tapes, audited returns, stress-test results, and default recovery data. Sound due diligence serves all three goals, but the emphasis and depth differ meaningfully depending on your situation.

How Blue Bay Fund Approaches Investment Due Diligence

Investment due diligence is a structured, evidence-based process that evaluates an investment's viability, risks, and alignment with your financial objectives before capital is committed. It replaces guesswork with systematic analysis: verifying collateral, scrutinizing track records, stress-testing assumptions, and establishing monitoring protocols that continue long after the initial commitment.

For accredited investors, due diligence is not optional. It is the mechanism by which you distinguish well-managed funds from poorly structured ones, realistic return projections from marketing-driven ones, and genuine capital preservation strategies from superficial reassurances. A disciplined process protects your principal, reduces surprises, and significantly improves the probability of achieving your target returns across varying market conditions.

The form that due diligence takes should match who you are as an investor. A pre-retiree prioritizing monthly income needs to scrutinize collateral quality, distribution sustainability, and principal protection mechanisms. A busy professional with limited time needs a framework that delivers rigorous answers efficiently, without demanding weeks of research. A sophisticated allocator building a diversified alternatives portfolio needs deal-level transparency: loan tapes, audited returns, stress-test results, and default recovery data. Sound due diligence serves all three goals, but the emphasis and depth differ meaningfully depending on your situation.

See our distribution history and collateral standards — download the Blue Bay Fund I overview.

How Blue Bay Fund Approaches Investment Due Diligence

Before walking through the full due diligence framework, it helps to see what disciplined investment due diligence looks like in practice. Blue Bay Fund I is built around three integrated pillars that directly address the core concerns of income-seekers, time-constrained professionals, and sophisticated allocators.

The foundation is conservative underwriting. Every loan in the portfolio is evaluated against strict loan-to-value thresholds, supported by independent property appraisals, and informed by thorough borrower credit analysis. This discipline ensures that every risk accepted is fully understood, fairly priced, and protected by meaningful collateral equity. It is what allows the fund to offer reliable distributions without taking on the structural leverage that creates catastrophic downside in adverse markets.

The second pillar is a multi-layered risk assessment model integrating market trend analysis, individual borrower credit evaluation, and rigorous stress testing under diverse economic scenarios. This proactive framework identifies vulnerabilities early, before they appear in reported performance metrics, and enables timely portfolio adjustments that protect capital before problems compound.

The third pillar is transparent investor communication. Investors receive timely, accurate updates on portfolio performance, individual loan status, and distribution schedules. For income-seekers who need consistent reassurance that their capital is working safely, and for busy professionals who want clarity without complexity, reliable reporting is not a secondary concern. It is a fundamental component of the trust relationship between a fund manager and its investors.

If your priority is reliable monthly income and capital safety, download the Blue Bay Fund I overview to see our distribution history and collateral standards. [Insert link]

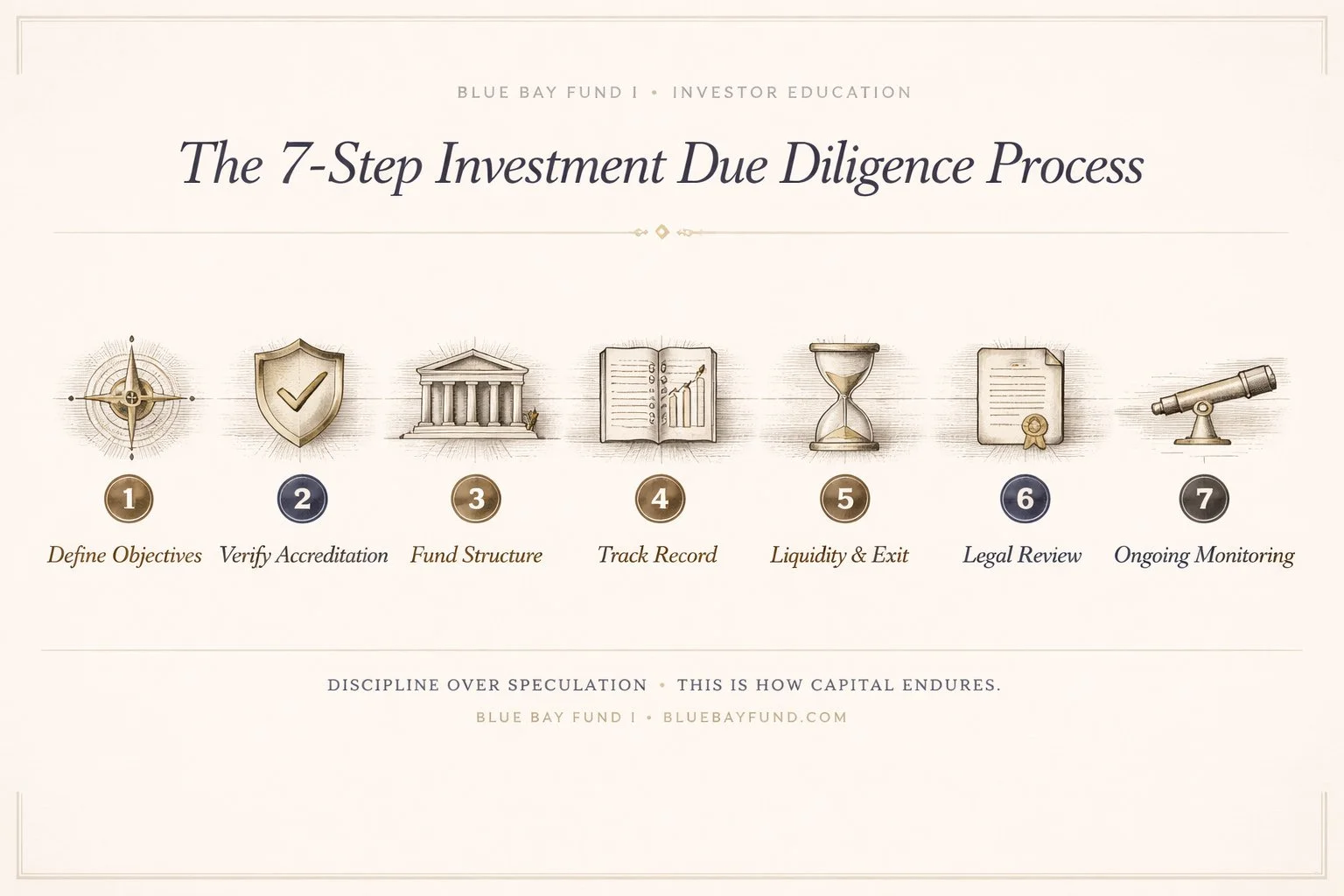

Key Steps in Conducting Effective Investment Due Diligence

Effective due diligence follows a clearly defined sequence. Skipping steps or compressing the process under time pressure is one of the most common and most costly mistakes accredited investors make. The following steps apply to any private investment, with particular relevance to real estate-backed funds and senior secured notes.

Step 1: Define Your Investment Objectives

Before evaluating any specific opportunity, clarify what you need the investment to accomplish. Are you prioritizing reliable monthly distributions, long-term capital growth, or above all else, protection of principal? What is your risk tolerance, and how does this investment fit within your broader portfolio? Investors who skip this foundational step often end up in technically sound investments that are wrong for their personal situation: generating income they do not need, locking up capital they cannot afford to have illiquid, or carrying risk that keeps them awake at night.

Step 2: Verify Accreditation and Eligibility

Confirm that you meet the accreditation requirements for the specific offering you are evaluating. Accreditation status governs access to private placements and significantly shapes your available investment universe. Prepare your documentation early, not only because it is required, but because doing so signals to fund managers that you are a serious, qualified investor who understands the regulatory framework in which private offerings operate.

Step 3: Evaluate Fund Structure and Governance

Before analyzing returns, understand how the fund is legally and operationally structured. Is your capital deployed in a senior secured position, or are you subordinated to other creditors? What are the loan-to-value thresholds on collateralized assets? How are distributions funded: from operating income or from returned investor capital? Are there independent administrators, auditors, or loan servicers providing oversight that is separate from the fund manager? These governance questions determine whether the structure is built to protect investors or primarily to serve manager interests.

Step 4: Analyze the Track Record

Request historical performance data at both the manager and individual asset levels. Go beyond headline return figures. Examine consistency of performance across different market environments, drawdown history, default rates on underlying loans, and recovery outcomes when defaults did occur. A manager who has successfully navigated a full market cycle, including a period of economic stress, provides meaningfully more confidence than one with only a short bull-market track record. Audited financials, third-party verified data, and independently administered performance records carry far more weight than manager-prepared summaries.

Step 5: Assess Liquidity and Exit Options

Clarify holding periods, redemption windows, and secondary market availability before making any capital commitment. This step is particularly critical for investors whose circumstances may change, including a pre-retiree who may need capital access for healthcare costs, or a busy professional whose income situation could shift unexpectedly. Understanding exactly when and how you can exit an investment, and at what cost, is not pessimism. It is prudent capital management.

Step 6: Review Legal Documentation

Carefully read the Private Placement Memorandum, Operating Agreement, subscription documents, and any side letters or amendments. Pay close attention to fee structures at every level, manager compensation arrangements, conflict-of-interest disclosures, conditions under which investment terms can be modified, and what recourse investors have if the manager underperforms or breaches their obligations. For significant capital commitments, engaging independent legal counsel to review documentation is a worthwhile investment in its own right.

Step 7: Establish Ongoing Monitoring

Due diligence does not end at the moment of investment. Establish a monitoring schedule: formal reviews at minimum annually, and a more immediate review following any material event affecting the fund or its underlying assets. Consistent monitoring allows early detection of performance deviations, management changes, or market shifts that warrant portfolio adjustments before small problems compound into significant losses.

Investment Due Diligence for the Time-Constrained Investor

For doctors, lawyers, executives, and business owners, the central due diligence challenge is rarely sophistication. It is time. You have the financial acumen to evaluate an investment rigorously, but not the bandwidth to spend evenings in spreadsheets or weekends on investor calls. This constraint does not require you to lower your standards. It requires you to focus your limited time on the questions that matter most for your specific situation.

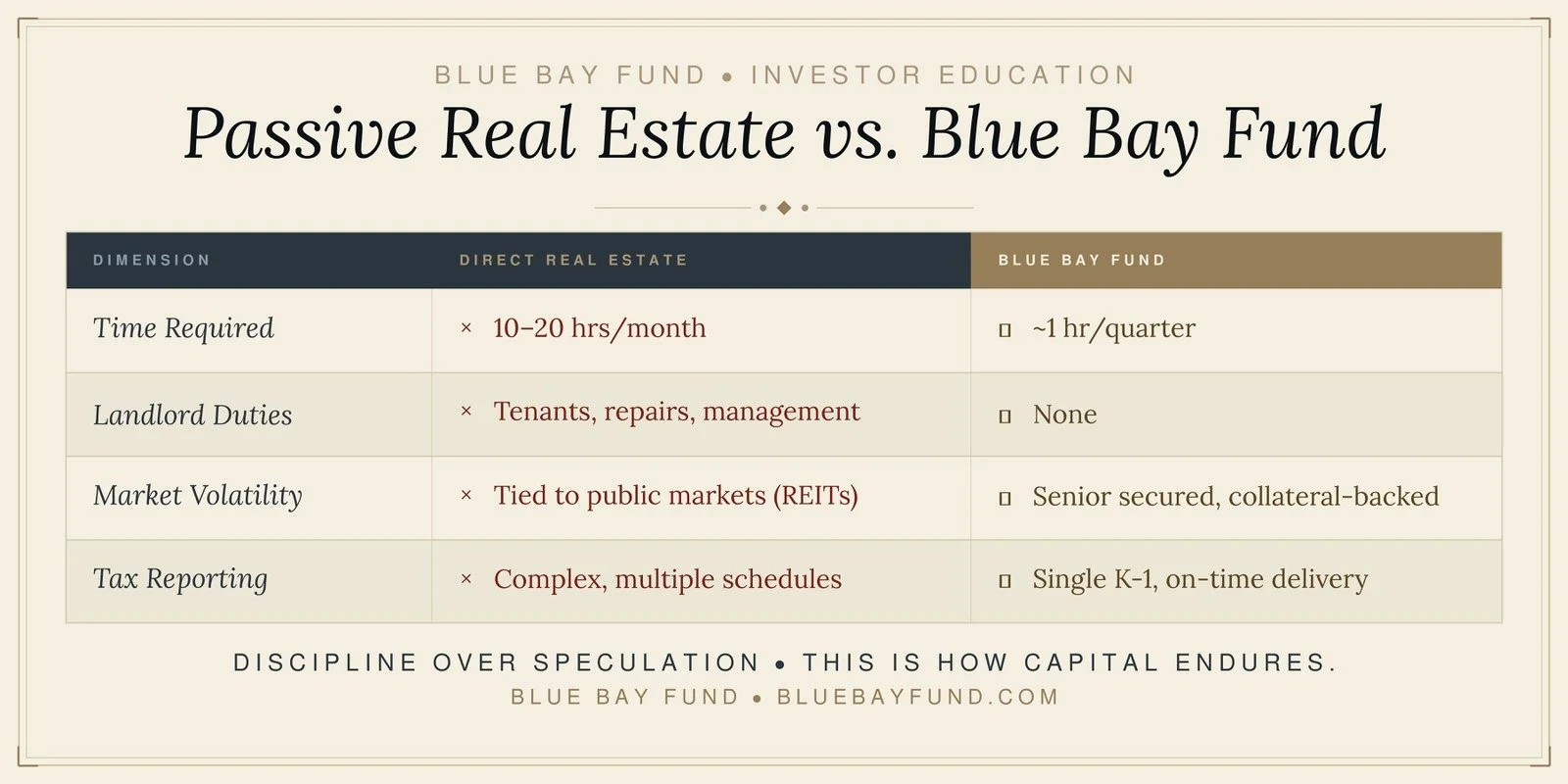

I earn well but I have zero time. I want real estate exposure without being a landlord or spending weekends on it.

The single most important question for a time-constrained investor is not what the projected return is. It is how passive the investment truly is after the commitment is made. A well-structured real estate debt fund should require essentially zero ongoing involvement from investors beyond reviewing periodic reports. The fund manager handles loan origination, underwriting, servicing, monitoring, and investor reporting. Independent administrators and servicers provide oversight. You receive distributions and quarterly updates, not calls about roof repairs or tenant disputes.

When evaluating any opportunity for true passivity, confirm that distributions are contractually scheduled and funded from operating income rather than returned capital. Verify that an independent fund administrator and loan servicer are in place, separate from the fund manager, so that operational risk does not rest on any single person or team. Understand the tax reporting process clearly, specifically when K-1s are delivered and how your CPA will be supported through reporting season. Request references from investors with professional backgrounds similar to yours, because a peer referral from a fellow physician or executive carries far more meaningful validation than a generic testimonial.

The goal of this focused approach is not to shortcut rigor. It is to concentrate your analytical effort on the dimensions that matter most for a passive, income-oriented investment. A fund that cannot answer these questions clearly, quickly, and without defensiveness is signaling something important about its transparency and operational quality, regardless of how attractive its headline numbers appear.

See how Blue Bay Fund investors receive monthly distributions with zero active management required. Schedule a 20-minute call with our investor relations team. [Insert link]

How to Perform Alternative Investment Risk Assessment

Alternative investments, including private real estate funds, senior secured mortgage notes, and private credit vehicles, require specialized risk evaluation that goes beyond standard equity or mutual fund analysis. The risk profile of these instruments is fundamentally different: illiquidity risk, concentration risk, counterparty risk, and operational risk all demand dedicated attention that generic due diligence frameworks often fail to address.

Financial Risk Assessment

Analyze cash flow projections with a skeptical eye toward the assumptions underlying them. Conservative due diligence means stress-testing the model under adverse scenarios: rising vacancy rates, declining property values, borrower defaults, and interest rate movements that affect debt service capacity. A credible fund manager will not only welcome this analysis but will have already conducted it internally and will share the results transparently. Resistance to scenario analysis, or overly optimistic base-case assumptions with no downside modeling, is itself a meaningful red flag that deserves serious weight in your evaluation.

Operational Risk Assessment

Evaluate the depth and quality of the management team, the robustness of internal controls, and the sophistication of the technology infrastructure supporting portfolio management and investor reporting. Operational risk, characterized by poor reporting systems, excessive key-person dependency, high staff turnover, or inconsistent internal processes, often predicts financial problems before those problems surface in reported numbers. A fund that has not invested in its operational infrastructure has almost certainly not invested sufficiently in protecting your capital either.

Legal and Compliance Risk Assessment

Confirm that the fund manager holds appropriate regulatory licenses, has a clean disciplinary history with relevant regulators, and that the fund itself is compliant with applicable securities laws and reporting obligations. Review material litigation history for both the manager and the fund. For real estate-backed funds specifically, verify title integrity, adequate insurance coverage, and environmental compliance across underlying assets. Gaps in any of these areas can create liability that ultimately affects investor returns.

Counterparty Risk Assessment

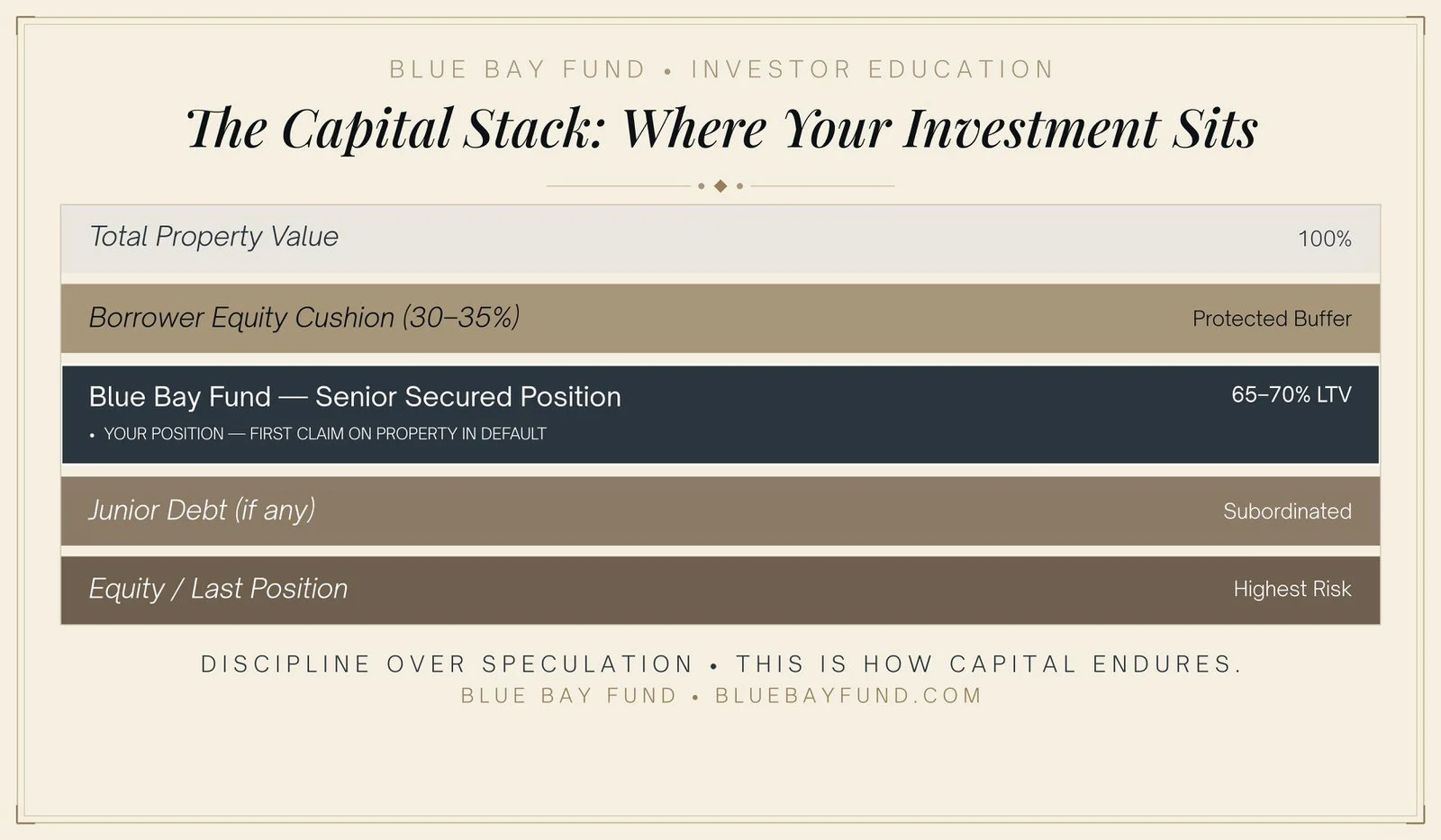

In real estate debt funds, the borrower is a primary counterparty whose quality directly affects your risk exposure. Evaluate borrower creditworthiness, relevant experience, and the equity they have contributed to the underlying transaction. Borrowers with meaningful equity contributions have strong incentives to service their debt obligations and protect the asset. First-position mortgage notes provide the strongest counterparty protection structure: in the event of borrower default, senior secured lenders hold priority claim on the underlying property, providing a clearer and more predictable recovery pathway than subordinated debt or equity positions.

Evaluating Real Estate-Backed Investment Opportunities

Real estate-backed investments demand meticulous asset-level scrutiny before capital deployment. Unlike publicly traded REITs, where liquidity and price transparency come at the cost of market volatility correlation, private real estate funds offer direct collateral protection, but only when that collateral has been properly underwritten, documented, and independently verified.

The loan-to-value ratio is the foundational metric in real estate debt evaluation. Conservative funds maintain LTV thresholds below 65 to 70 percent, providing meaningful equity cushion between the outstanding loan balance and the property value. This buffer is what protects principal in adverse scenarios: even if property values decline moderately, the fund's recovery position remains intact. Alongside LTV, the debt service coverage ratio confirms that property income sufficiently covers loan payments under both base-case and stress conditions. Independent appraisals, title insurance, and property condition reports should be available for investor review. Their absence or inaccessibility is a serious structural concern.

Borrower equity contribution deserves particular attention. When borrowers have invested significant equity of their own, their incentive alignment with the lender is strong: they stand to lose materially from default, which powerfully motivates performance. Low or zero equity contributions from borrowers increase default probability and reduce recovery outcomes. This is a dimension that marketing materials rarely highlight but that experienced due diligence practitioners evaluate carefully.

The Capital Preservation Advantage of First-Position Notes

For income-focused investors whose primary concern is protecting principal while generating reliable distributions, first-position mortgage notes offer a structurally superior risk profile relative to subordinated debt or equity. As a senior secured lender, you hold the first claim on the underlying property in the event of default. Your recovery pathway is clearer, your loss exposure is bounded, and your position in the capital structure prioritizes your interest before junior creditors or equity holders receive anything.

This structural advantage does not eliminate risk. No investment does. But when combined with conservative LTV underwriting, independent oversight, and a demonstrated track record of disciplined asset management, first-position senior secured notes represent one of the most effective structures available for delivering reliable income alongside meaningful capital protection.

The Role of Wealth Managers and Professional Advisors in Due Diligence

Wealth managers serve as trusted gatekeepers for accredited investors, evaluating opportunities rigorously, aligning incentives with client interests, and providing ongoing portfolio oversight across market cycles. Their value is greatest when they operate as true fiduciaries, legally required to act in your best interest rather than simply meeting a lower suitability standard. Understanding which standard your advisor is held to is itself an important due diligence question.

The most valuable advisors in the alternative investment space conduct their own independent due diligence rather than relying solely on fund marketing materials. They scrutinize the same structural, operational, and legal dimensions discussed throughout this guide, applying specialized expertise in private real estate or alternative credit that a generalist advisor may lack. When evaluating an advisory relationship for private investment guidance, ask directly how the advisor is compensated in connection with the opportunities they recommend. Referral fees or revenue-sharing arrangements with fund managers create conflicts that deserve transparent disclosure and careful consideration.

Best Practices for Wealth Managers in Risk Management

Leading wealth managers protect client capital by applying conservative underwriting standards consistently, concentrating on structured income investments with predictable and income-funded cash flows, and maintaining rigorous awareness of the regulatory environment in which their clients' investments operate. The best advisors build repeatable processes rather than one-off evaluations: systematic frameworks applied consistently across multiple opportunities and market cycles, reducing the influence of enthusiasm, momentum, or marketing pressure on investment decisions.

How to Evaluate the Best Wealth Managers for Alternative Investment Due Diligence

For accredited investors evaluating wealth managers who specialize in alternative investment due diligence, the selection criteria are specific. The right manager will have a documented process for evaluating private credit and real estate-backed funds, a track record across multiple market cycles, and a transparent compensation structure that eliminates conflicts of interest. Credentials alone are not sufficient. What distinguishes the best wealth managers for alternative investment due diligence is a repeatable, evidence-based process that holds up to scrutiny on every deal, not just the ones that performed well.

Blue Bay Fund works directly with wealth managers and their clients to provide the deal-level transparency and reporting infrastructure that rigorous alternative investment due diligence requires. If you are a wealth manager evaluating private real estate debt funds on behalf of accredited investor clients, we welcome the conversation and will provide the documentation, performance history, and loan-level data your process demands.

Capital Preservation Strategies for Alternative Investments

Capital preservation is not simply about avoiding obvious losses. It is about structuring investments so that downside scenarios are predictable, bounded, and manageable before they occur. The most effective capital preservation strategies combine structural protections built into the investment itself with disciplined selection criteria applied consistently by the investor.

Senior secured positioning is the structural foundation of capital preservation in real estate debt investing. By maintaining priority claim on underlying assets, senior secured investors dramatically improve their recovery position in adverse scenarios relative to investors in subordinated or equity structures. Conservative LTV underwriting, ideally below 65 percent, reinforces this protection by ensuring that meaningful property equity sits between the loan balance and any potential loss. Diversification across multiple loans and properties within a fund further reduces the impact of any single asset's underperformance on overall portfolio results.

Manager selection is equally important. Prioritize managers who provide transparent, consistent reporting verified by independent third parties. Avoid investments where projected yields significantly exceed comparable market rates without clear structural justification, since outlier returns almost always reflect outlier risk, whether or not that risk is disclosed prominently in the offering documents.

Integrating Passive Income Goals with Due Diligence

The most effective approach to income-oriented investing aligns your income objectives directly with your due diligence framework from the outset. Define your monthly income target with specificity, then evaluate whether the fund's historical distribution record is consistent with that target across varying market conditions. Confirm that distributions are funded from operating income rather than return of capital, a critical distinction that marketing materials frequently obscure. Establish a regular portfolio review cadence that keeps your investment aligned with your income needs without demanding the kind of constant attention that defeats the purpose of a passive investment strategy.

Request the Blue Bay Fund I offering documents, sample loan tape, and audited performance history.

About Blue Bay Fund

Blue Bay Fund is a recognized leader in real estate-backed investment opportunities with extensive expertise in underwriting, asset management, and investor relations. Blue Bay Fund delivers disciplined, transparent, and professionally managed solutions designed specifically for accredited investors, whether your priority is reliable monthly income, truly passive real estate exposure, or institutionally structured returns backed by senior secured collateral.

Blue Bay Fund's rigorous due diligence protocols, conservative underwriting standards, and comprehensive investor reporting are built to generate sustainable passive income while prioritizing the capital preservation that accredited investors depend on. For more information, visit Blue Bay Fund.

Edwin D. Epperson III Fund Manager · Blue Bay Fund I

Edwin D. Epperson III is a former U.S. Army Green Beret, Ranger School and Combat Diver qualified, who has deployed over $30 million into more than 150 secured, real estate-backed investments over his career. He founded Blue Bay Fund I on the same principles he led with in Special Forces: disciplined underwriting, full transparency with investors, and personal accountability through co-investment alongside every client.

Conclusion

Mastering investment due diligence is the foundation of confident, disciplined capital deployment, and it looks different depending on who you are as an investor. For a pre-retiree protecting a lifetime of savings, it means verifying collateral quality, distribution sustainability, and the structural safeguards that protect principal. For a busy professional seeking genuinely passive income, it means confirming that the investment requires nothing of your time after the commitment is made. For a sophisticated allocator demanding institutional-quality analysis, it means examining every layer of the structure until the numbers either hold up or they do not.

Blue Bay Fund is built to meet each of these standards. If you have read this guide and recognize the discipline it describes in how you want your capital managed, the logical next step is a direct conversation with our team.

Ready to Apply These Standards

to a Real Opportunity?

Schedule a call with Blue Bay Fund's investor relations team and receive our complete fund overview, distribution history, and underwriting standards.

Edwin D. Epperson III,

Manager & CEO

Soli Deo Gloria