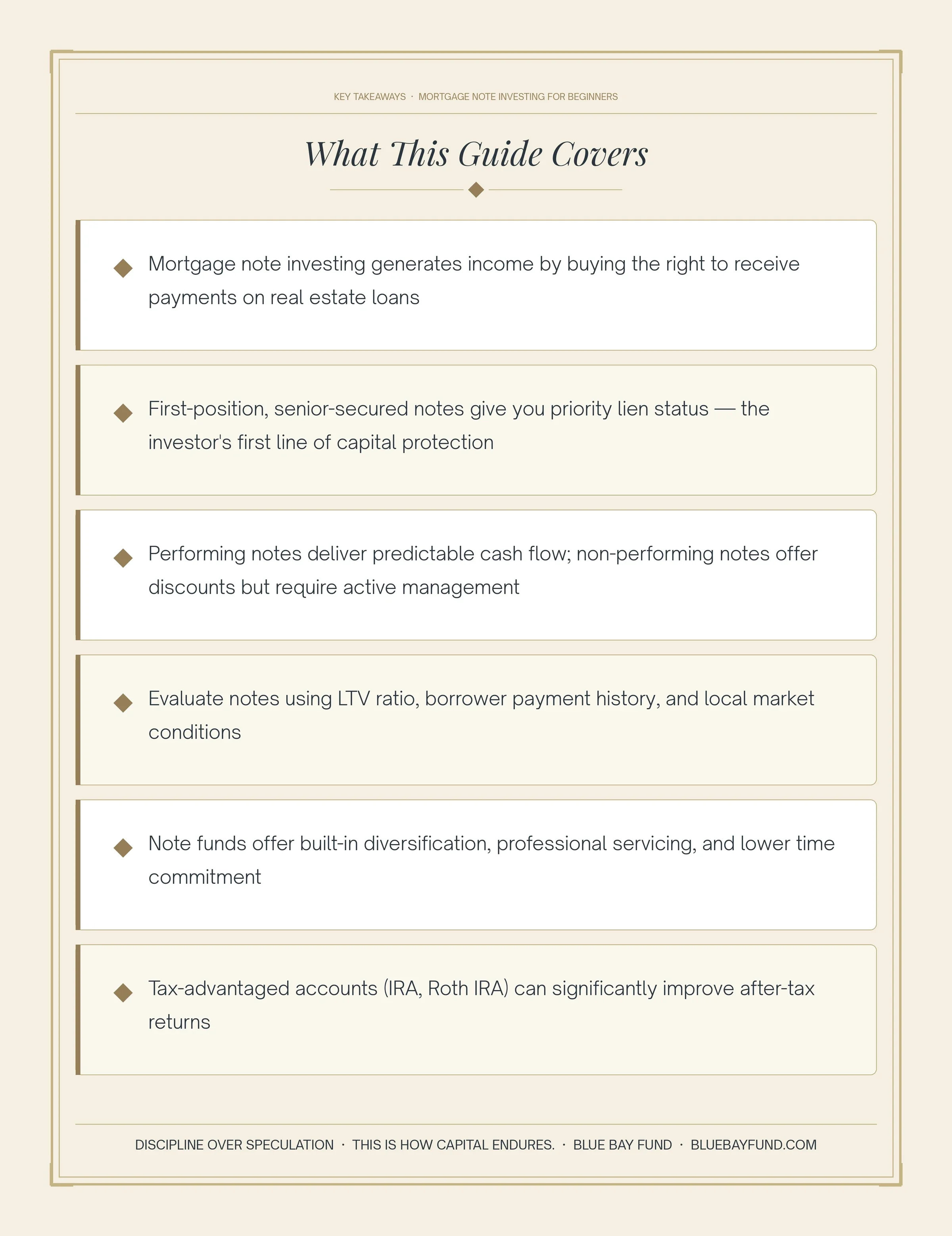

Mortgage Note Investing for Beginners: Lessons from 150+ Deals

Insights & Education · Blue Bay Fund

A practitioner's guide to buying the right to collect, without managing tenants, maintaining properties, or tying up capital in a single asset.

Most people learn about real estate investing through landlords, rentals, and fix-and-flips. But there is a quieter corner of the market, one where you hold the loan, not the property, that has consistently delivered passive income for investors who know where to look.

Mortgage note investing means buying the right to collect payments on an existing real estate loan. You step into the lender's position. The borrower keeps making monthly payments. You collect interest income, without managing tenants, maintaining a property, or tying up capital in a single physical asset.

With 150+ deals invested in Blue Bay Fund, we've seen what separates notes that perform reliably from those that cause headaches. This guide breaks down how note investing works, what to look for, and how accredited investors are using it to build disciplined passive income streams.

Earn Like the Lender

Step into predictable monthly income secured by real assets, without the burden of ownership.

What Is a Mortgage Note, and Why Would You Want to Own One?

A mortgage note is a legal document that records a borrower's promise to repay a real estate loan. It spells out the interest rate, payment schedule, and the property used as collateral. When a bank or private lender originates a mortgage, the note is the core asset, and that asset can be bought and sold on the secondary mortgage market.

When you buy a mortgage note, you are not buying the property. You are buying the income stream attached to it. The borrower continues living in their home and making payments, those payments now flow to you.

Think of it this way: owning a rental property is like owning a store. Owning a mortgage note is like owning the financing on that store. You get paid whether business is booming or slow, because your claim comes first.

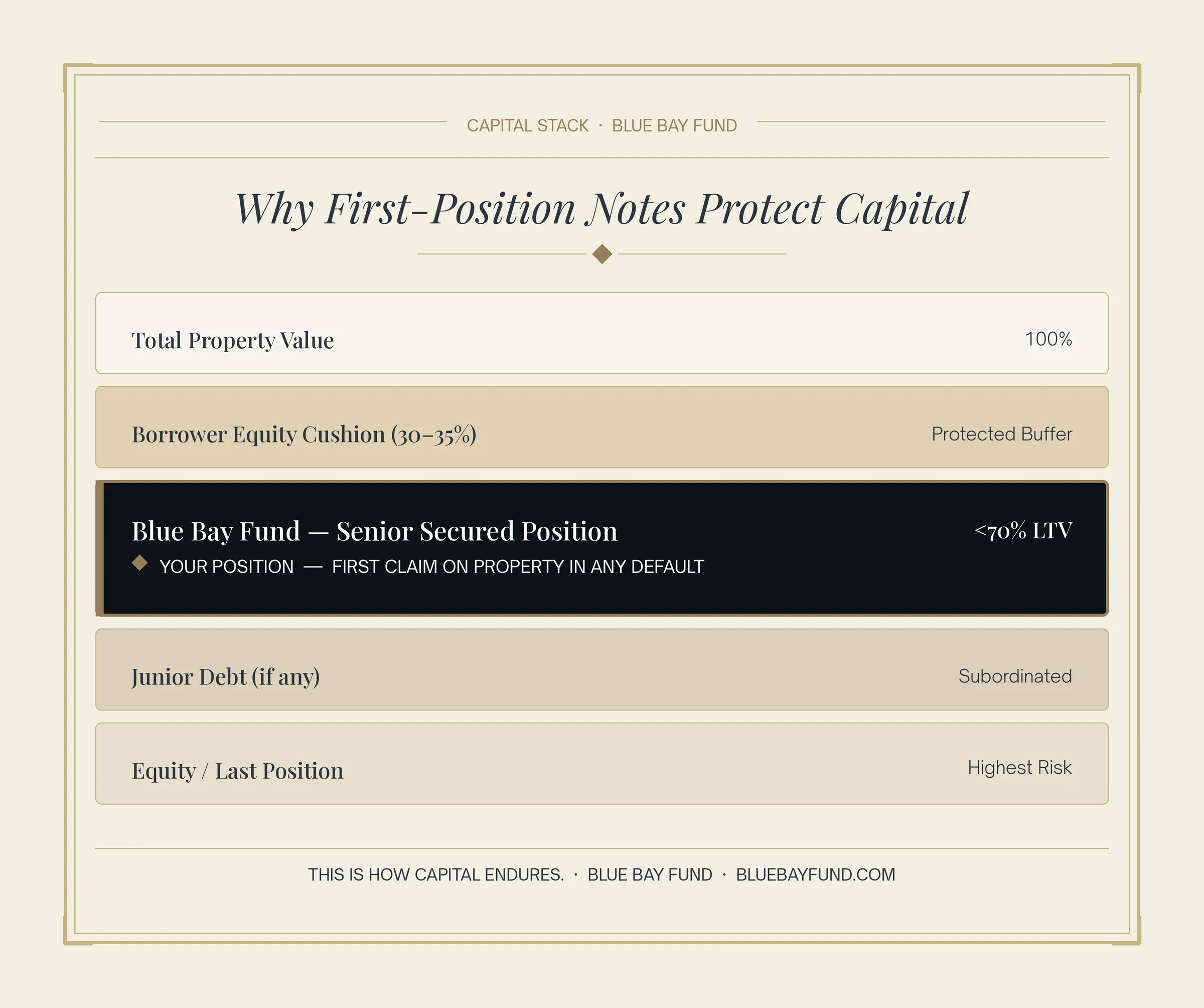

Why First-Position Notes Matter

A first-position mortgage note means your lien is senior to all others on the property. If a borrower defaults, note holders with first position have priority in any recovery over second liens, unsecured creditors, and equity holders. At Blue Bay Fund, we focus primarily on first-position, senior-secured notes, because the collateral structure is the investor's first line of capital protection.

Blue Bay Fund · First-Position Investing Principle.

How Mortgage Note Investing Generates Passive Income

The income mechanics are straightforward. You purchase a note at a price, either at par (face value) or at a discount, and you receive the borrower's monthly principal and interest payments for the remaining term of the loan. Your yield is determined by the note's interest rate, what you paid for it, and how long payments continue.

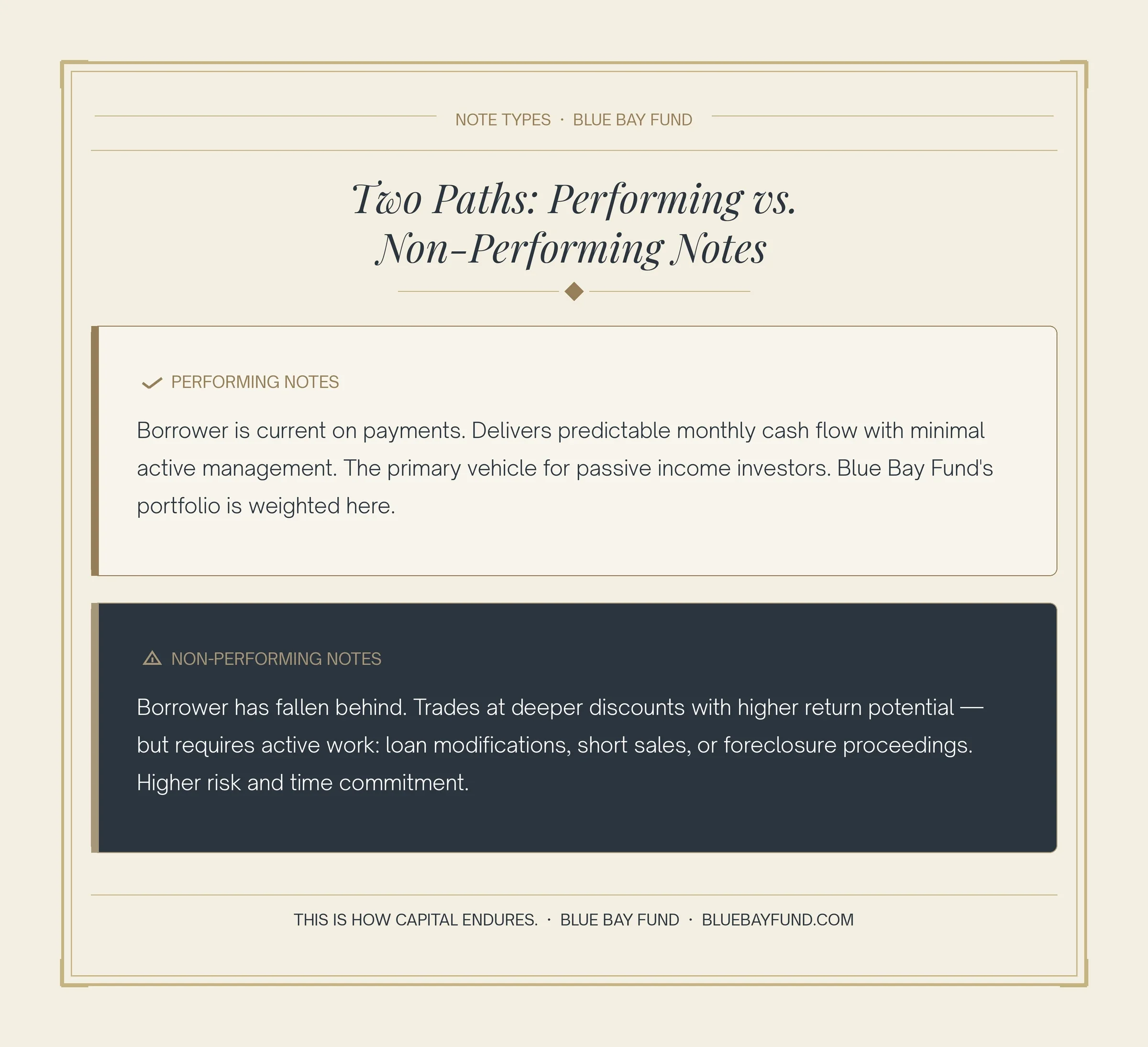

Performing vs. Non-Performing Notes

What Returns Look Like in Practice

Performing mortgage notes typically yield between 7% and 12% annually, depending on the note's interest rate, the loan-to-value (LTV) ratio, and the purchase discount. Non-performing note strategies can target higher returns, but the timeline and effort required are substantially greater.

If your priority is reliable monthly income and capital preservation, request access to the Blue Bay Fund I investor brief.

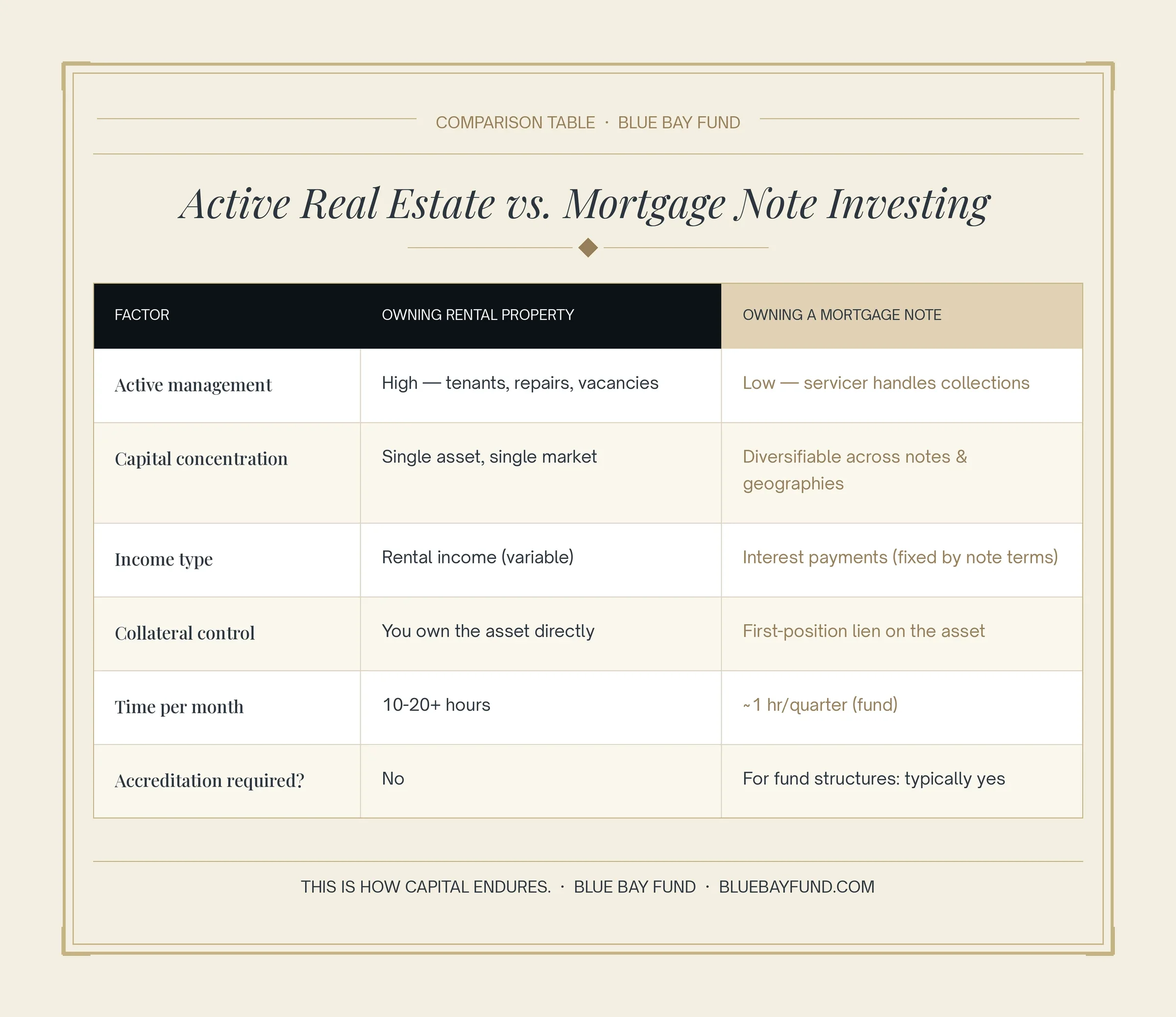

Mortgage Notes vs. Owning Property Directly: A Comparison That Changes How You Think About Real Estate

Most real estate investors default to the landlord model — buy a property, find tenants, collect rent, manage maintenance, repeat. It works. But the operational burden is real, and the capital is concentrated in a single asset.

Mortgage notes change the equation significantly:

The practical implication: a note investor with $500,000 in capital can diversify across 5–10 separate notes in different states, with different borrowers and different property types, reducing concentration risk that a single rental property investor simply cannot achieve.

See how Blue Bay Fund investors receive monthly distributions with zero active management required. Schedule a 20-minute call with our investor relations team.

How to Evaluate a Mortgage Note: The Due Diligence Checklist

Not all notes are created equal. Evaluating one properly requires looking at four interconnected factors:

How Blue Bay Fund Approaches Mortgage Note Investing

Blue Bay Fund I was built around a simple discipline: acquire first-position, senior-secured performing notes at prices that provide a margin of safety, and manage the portfolio with active monitoring that catches problems early.

After 150+ deals, the patterns that separate successful notes from costly ones are remarkably consistent. The variables never change, only the investors who ignore them do.

Blue Bay Fund · Portfolio Management Principles.

After 150+ deals, the patterns that separate successful notes from costly ones come down to a few consistent variables:

Lessons from the Deal Floor

Deals where we skipped title verification always created problems. Always. No exceptions. Borrowers with 24+ months of clean payment history on performing notes almost never default without a major external shock — job loss, divorce, illness. Even then, the conversation usually leads to modification rather than foreclosure. Markets matter more than individual property quality. A well-maintained home in a declining market is harder to exit than a modest home in a growing one. Diversification is the single most reliable risk management tool available. No individual note, regardless of how clean it looks, should represent more than 10–15% of a portfolio.

Our underwriting process layers these lessons into every acquisition: LTV screening, borrower history verification, title review, servicer due diligence, and market assessment — before any capital is committed.

On Tax Structure

Who Is Mortgage Note Investing Right For?

Mortgage note investing through a fund structure like Blue Bay Fund I is designed for accredited investors, those who meet SEC income or net worth thresholds, who are looking for:

Predictable passive income without the operational demands of property management.

Portfolio diversification beyond stocks, bonds, and traditional real estate equity.

A real estate-backed alternative investment with defined collateral and senior lien position.

Tax-advantaged income potential when structured through qualifying retirement accounts.

It is not the right fit for investors who need short-term liquidity, are seeking speculative growth, or are uncomfortable with the illiquid nature of private credit investments. Note investing rewards patience and discipline, not velocity.

Request Access to the Blue Bay Fund I Investor Brief

Access offering documents, sample loan tape, and distribution history.

Available to accredited investors upon request.

Frequently Asked Questions

Difference between a mortgage note and a deed of trust

A mortgage note is the borrower’s promise to repay a loan, while a deed of trust secures that loan with the property as collateral. In note investing, you acquire both the income stream and the legal right to enforce the lien if the borrower defaults.

Can I invest in mortgage notes through an IRA?

Mortgage notes can be held inside self-directed IRAs and Solo 401(k)s, allowing investors to generate tax-deferred or potentially tax-free income. These accounts can also invest in note funds like Blue Bay Fund I, provided the structure is set up correctly with a qualified custodian.

What happens if a borrower stops paying on a note I own?

If a borrower stops paying, note investors typically pursue a loan modification first, followed by foreclosure if necessary. Loan modifications can restore performing status more efficiently, while foreclosure allows recovery of the underlying collateral if the borrower cannot resume payments.

How liquid are mortgage note investments?

Mortgage note investments are relatively illiquid and are best suited for medium- to long-term holding periods. While individual notes can be sold on the secondary market, transactions may take weeks or months, and fund investments often have defined hold periods.

What returns can I realistically expect from mortgage note investing?

Mortgage note investments typically generate 7 to 12 percent annual returns, depending on note quality, purchase price, and portfolio management. Performing notes provide stable income, while non-performing strategies can offer higher returns with increased complexity and risk.

Is mortgage note investing safe?

Mortgage note investing can be relatively safe when backed by real estate and structured with conservative loan-to-value ratios. First-position notes provide collateral protection, but risks remain, including borrower default, market fluctuations, and limited liquidity.

How do beginners start investing in mortgage notes?

Beginners typically start mortgage note investing through funds or partnerships with experienced operators. This approach offers diversification, professional management, and access to deal flow without needing to source or service loans directly.

About Blue Bay Fund

Blue Bay Fund is a recognized leader in real estate-backed investment opportunities with extensive expertise in underwriting, asset management, and investor relations. Blue Bay Fund delivers disciplined, transparent, and professionally managed solutions designed specifically for accredited investors, whether your priority is reliable monthly income, truly passive real estate exposure, or institutionally structured returns backed by senior secured collateral.

Blue Bay Fund's rigorous due diligence protocols, conservative underwriting standards, and comprehensive investor reporting are built to generate sustainable passive income while prioritizing the capital preservation that accredited investors depend on.

Getting Started: The Disciplined Path into Mortgage Note Investing

Mortgage note investing is not a shortcut. It rewards investors who take the time to understand the mechanics, do the due diligence, and build a diversified portfolio with real capital protection at its foundation.

The investors who do it well share a few common habits: they verify everything, they diversify early, they work with experienced servicers, and they stay patient through the income-building process.

Blue Bay Fund I was built to make that process accessible to accredited investors who want senior-secured, first-position note exposure without building their own deal-sourcing and underwriting infrastructure from scratch.

Disciplined leadership. Structured for capital protection.

Edwin D. Epperson III, Chief Investment Officer of Blue Bay Fund I, leads with a focus on conservative underwriting, first-position collateral, and predictable income generation. His background as a Green Beret and operator informs a disciplined, risk-first investment approach.

Investors gain access to a strategy built on capital preservation, structured downside protection, and long-term performance.

Edwin D. Epperson III,

Manager & CEO

Soli Deo Gloria