What are Private Notes

In this article, I discuss the primary types of notes. This is not conclusive, and there are many niches in note investing. My goal is not to compare all kinds of note investing but to compare the two primary types. That would be secured note investing and unsecured note investing. In this video, I go over the differences between the two and why investing in notes secured to hard, tangible assets is the safest and most risk-mitigated way to invest in notes. I also go over why investing in notes secured to real estate is the safest way to invest in notes.

I hope you enjoyed the video! Below are the primary slides from the presentation and a brief description of what is discussed in the video. If you have questions, scroll to the bottom of the page and email me, or discover more about my Investor Club!

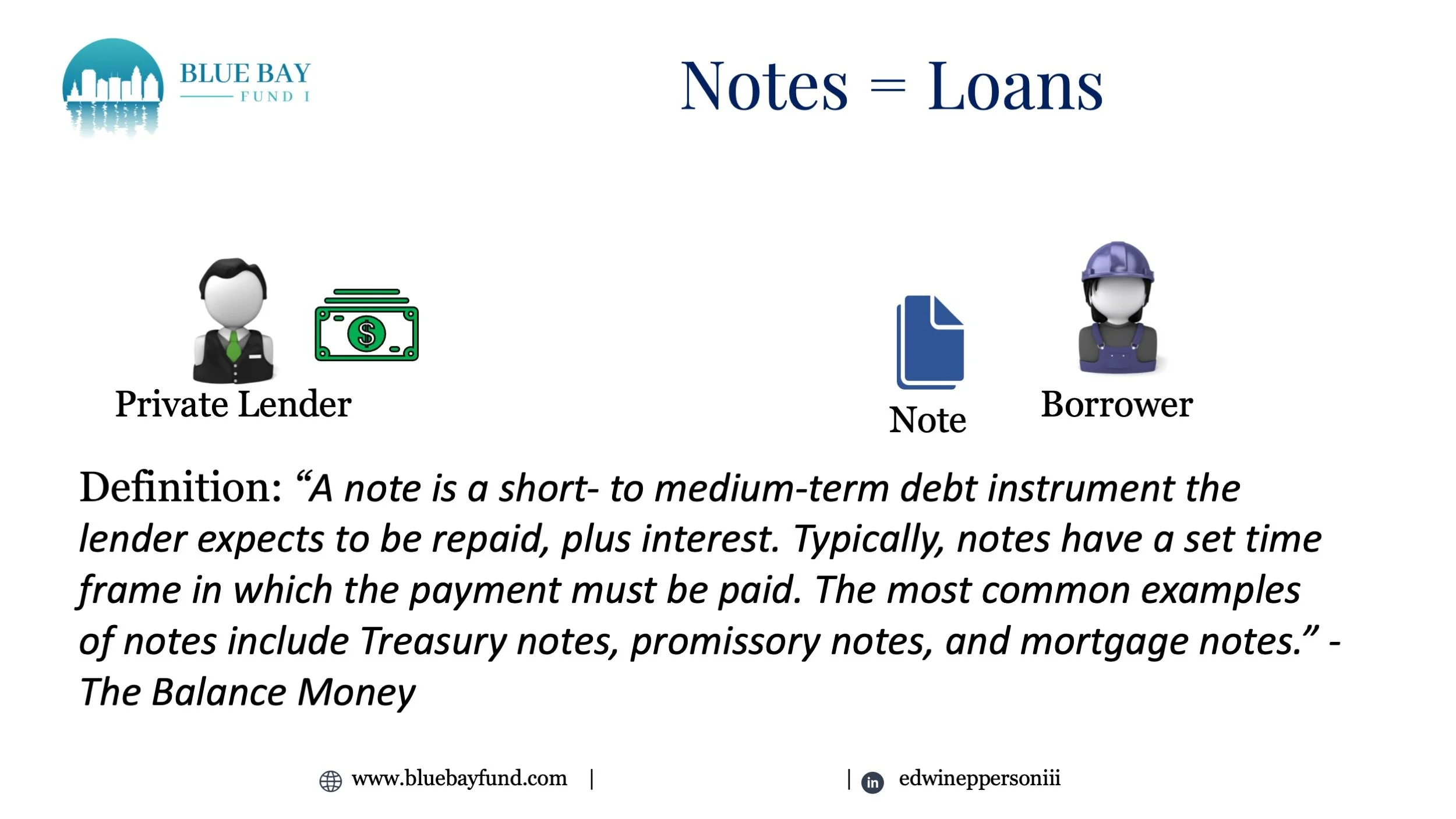

What is a note?

The definition of a note is quite simple. A note is a physical representation of your capital (the lenders) given to you by the borrower. The note tells all parties involved how much you are lending, the rate of return, when you should expect that note to be repaid, and the payment structure of the note. This is just like REAL money because it's a legally binding document, enforceable in court, representing the exact amount of money you loaned. Keep it secret, keep it safe.

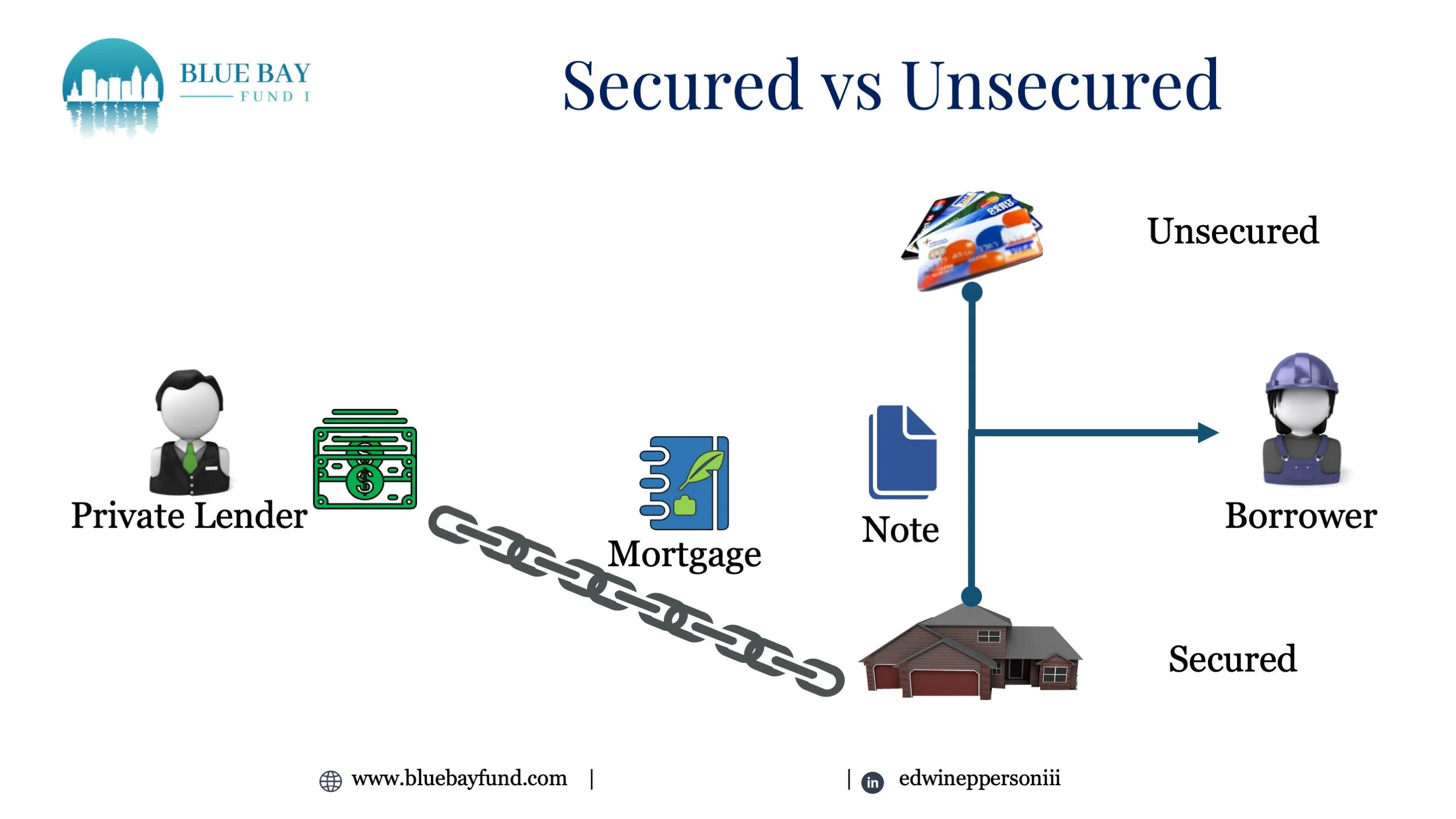

Secured or unsecured thats the question.

When investors make a loan and receive a note from the borrower, they may think that that note alone is all that is needed to “secure” their capital. I mean, the borrower personally signed the loan, right? However, we need to understand that lending has more nuances than simply getting a piece of paper signed by the borrower. The greatest tragedy in lending is when a lender thinks their loan is secured, but it is not.

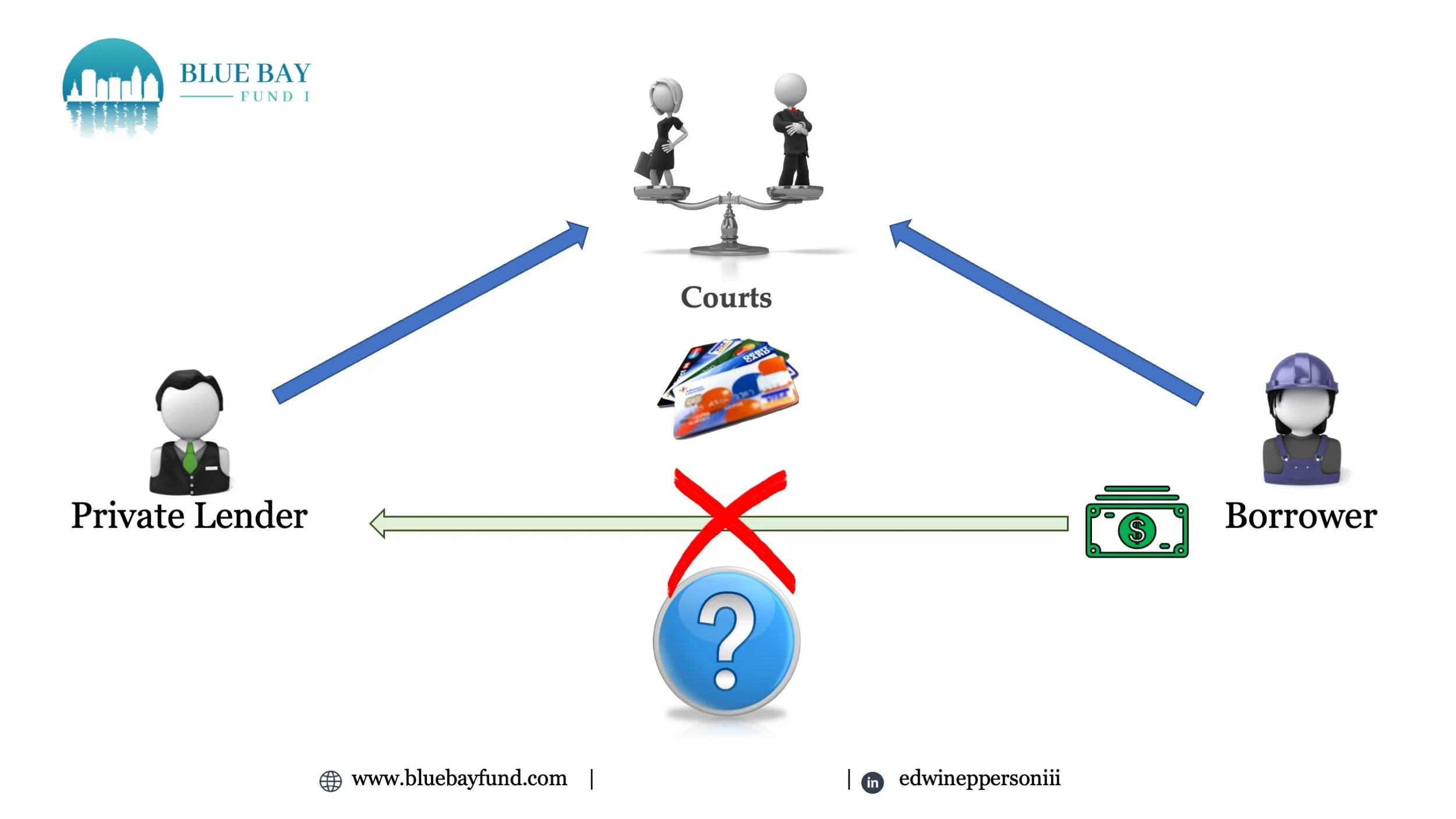

Whats the worst that could happen?

The worst that could happen is the borrower doesn’t pay, correct? Well, in the case of an “unsecured” loan, that worse case can be much… worse. Primarily because if the loan is unsecured (think of it as if you just gave the money to the borrower, and they went to Vegas to spend the money), then you must take the borrower to civil court. You will spend time and an obscene amount of money on attorneys, and it’s likely you will never see your principal balance again.

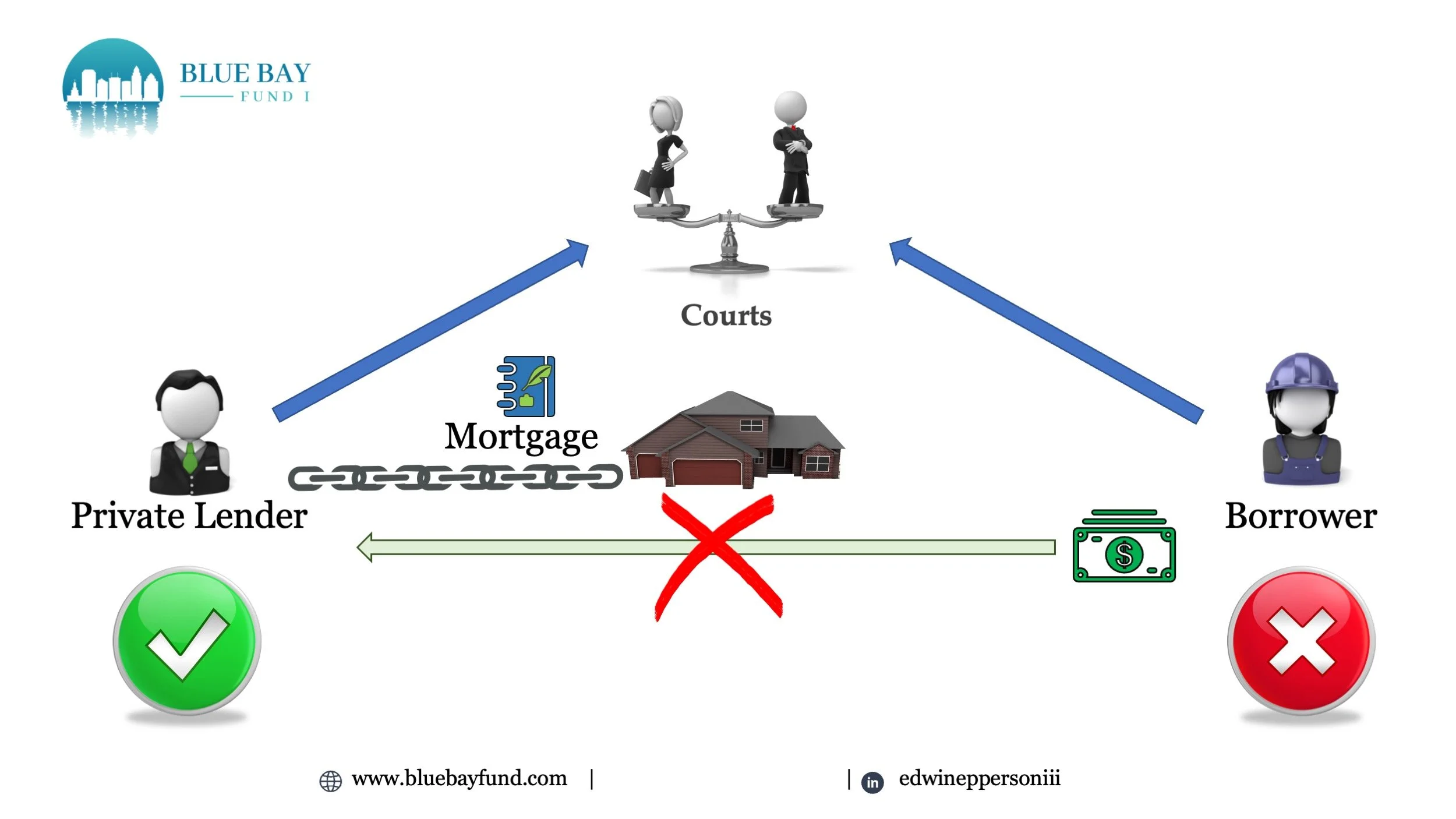

Security helps you sleep at night.

When your note is properly secured via a Mortgage or Deed of Trust (I discuss the differences in another video), you have the courts in your favor and have basically backed your borrower into a corner. They can fight it in court, and you both will rack up litigation fees; however, your properly secured note via the mortgage is what guarantees that you will own the property should you foreclose! If you have underwritten your file properly (meaning mitigated and shifted all risks), then you are in a great position.

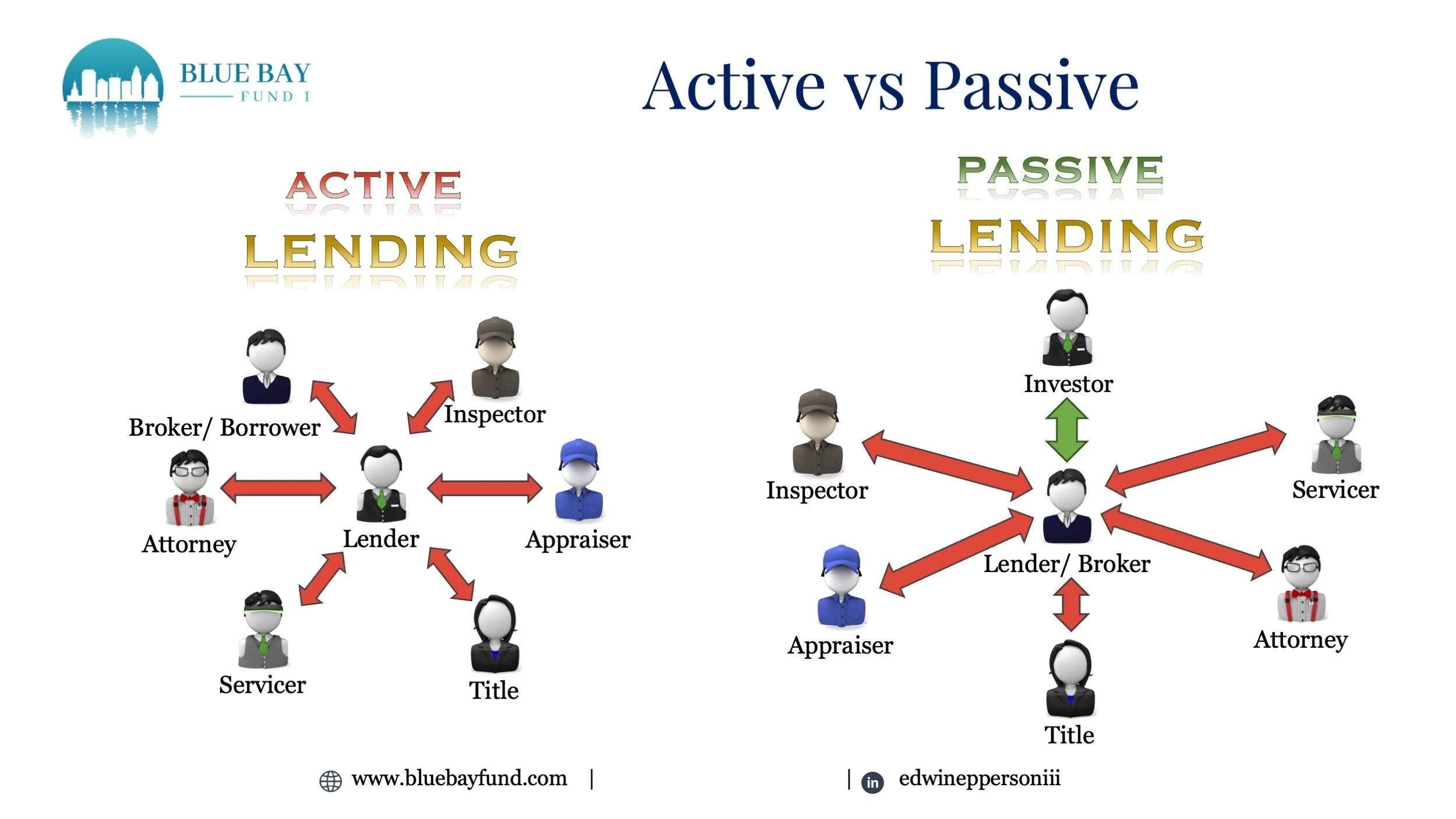

Decision point active or passive investor?

So, the question for you is, do you want to be a passive note investor or an active note investor? Being an active note investor takes time, knowledge, and experience. It will also put demands on you that are equivalent to another career. This is not for the part-time or faint of heart. Passive note investors, however, gain all the benefits of note investing without the requirements to build a business. Which one would you rather participate in?

So whether you have invested in private mortgages or deeds of trust, whether you have made secured loans or unsecured loans, the fact is there is a significant benefit to investing in notes secured to property.

Are you ready to consider investing in private investment notes secured to real estate? Are you looking for a risk-reduced strategy that will help you hedge against inflation while beating your average broker investment returns? Here is a better question: are you tired of paying fees for your investment advisors' “advice” even when you are losing value, but they still get paid?

I invite you to sign up and watch my presentation about the Blue Bay Fund and how we are helping investors make wiser, more informed decisions.

With Honor,

Edwin D. Epperson III,

Manager & CEO

Soli Deo Gloria