Unlocking Real Estate-Secured Private Credit Opportunities

Professional Photography: Carography Studios

Predictable income structured to protect capital and preserve long-term legacy.

Real estate‑secured private credit offers accredited investors predictable cash flow and downside protection via privately originated debt backed by tangible property. This article explores real estate‑backed lending, first‑position mortgage notes to real estate investors in capital preservation, and disciplined underwriting for steady income. We cover loan mechanics, benefits, market outlook for 2026, and values‑based stewardship for legacy‑focused allocations.

What Is Real Estate‑Secured Private Credit and How Does It Work?

Real estate‑secured private credit involves privately negotiated loans backed by a recorded property lien, granting lenders enforceable collateral rights upon default. First‑position liens ensure legal precedence, structuring clear recovery paths and lowering tail risk. These loans typically generate scheduled interest payments. Understanding lien mechanics and loan‑to‑value (LTV) limits clarifies how secured debt delivers predictable passive income while limiting downside exposure. Lenders employ title searches, insurance, and independent valuations, with conservative underwriting capping LTV to provide a protective equity cushion.

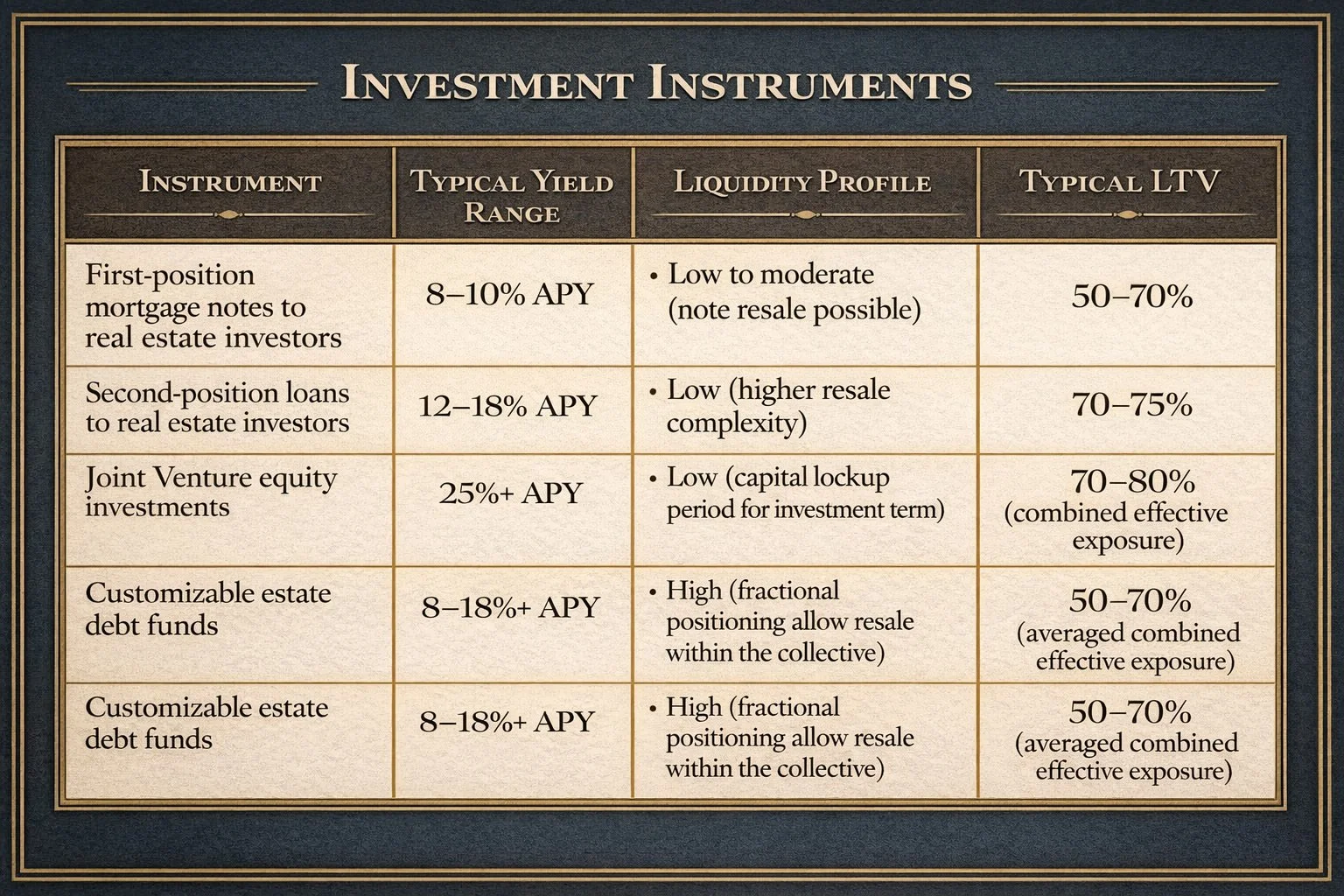

What Types of Real Estate‑Secured Investments Are Available?

Common real estate‑secured instruments include first‑position mortgage notes to real estate investors, 2nd position loans to real estate investors, joint venture equity investments, and customizable real estate debt funds, each with distinct risk‑return and liquidity. First‑position mortgage notes to real estate investors offer highest legal priority and direct collateral claim. 2nd position loans to real estate investors commands higher yield for added risk. Joint venture investments offer the highest yield, with the greatest risk to principal. Customizable debt funds spread idiosyncratic risk through a diversified approach across all three investment products. Comparing these options clarifies trade‑offs among yield, liquidity, and capital preservation, helping investors choose the instrument that fits their objectives.

Clarity and structure that help investors deploy capital with confidence.

What Are the Key Benefits of Investing in Real Estate Private Credit?

Real estate private credit delivers stability, predictable income, and collateral‑backed capital preservation—an appealing mix for accredited investors seeking lower volatility than paper markets and higher yields than public bonds. Contractual interest schedules create steady cash flow, while first‑position security and conservative LTVs reduce downside exposure. Real estate debt often shows low correlation with public equities, adding diversification.

Key investor benefits include:

Stability Through Collateral: Property collateral provides a tangible claim that limits loss severity.

Predictable Cash Flow: Contractual interest and repayment schedules create dependable income streams.

Diversification: Lower correlation with public markets can reduce overall portfolio volatility.

These advantages explain why disciplined private credit allocations attract investors focused on capital preservation and income. Different secured options involve trade‑offs for portfolio construction.

This comparison highlights how first‑position security and conservative LTVs generally trade lower yield for stronger downside protection, key for predictable income.

How Does Blue Bay Fund I Offer Unique Real Estate‑Secured Private Credit Opportunities?

Blue Bay Fund I, a faith‑informed steward, focuses on first‑position mortgage notes to real estate investors, and secondary focuses on second-position loans and joint venture equity investments. Through conservative underwriting for stability, steady cash flow, and legacy‑oriented stewardship for accredited investors, the fund emphasizes disciplined credit selection, secured collateralization, and active loan servicing, aligning return objectives with capital preservation. Founder Edwin D. Epperson III, a former U.S. Army Green Beret, applies a disciplined, mission‑oriented framework to investment decisions, emphasizing stewardship, integrity, and conservative risk management. Blue Bay Fund I has deployed over $35 million into over 170+ secured, real‑estate‑backed investments, informing its sourcing and underwriting playbook.

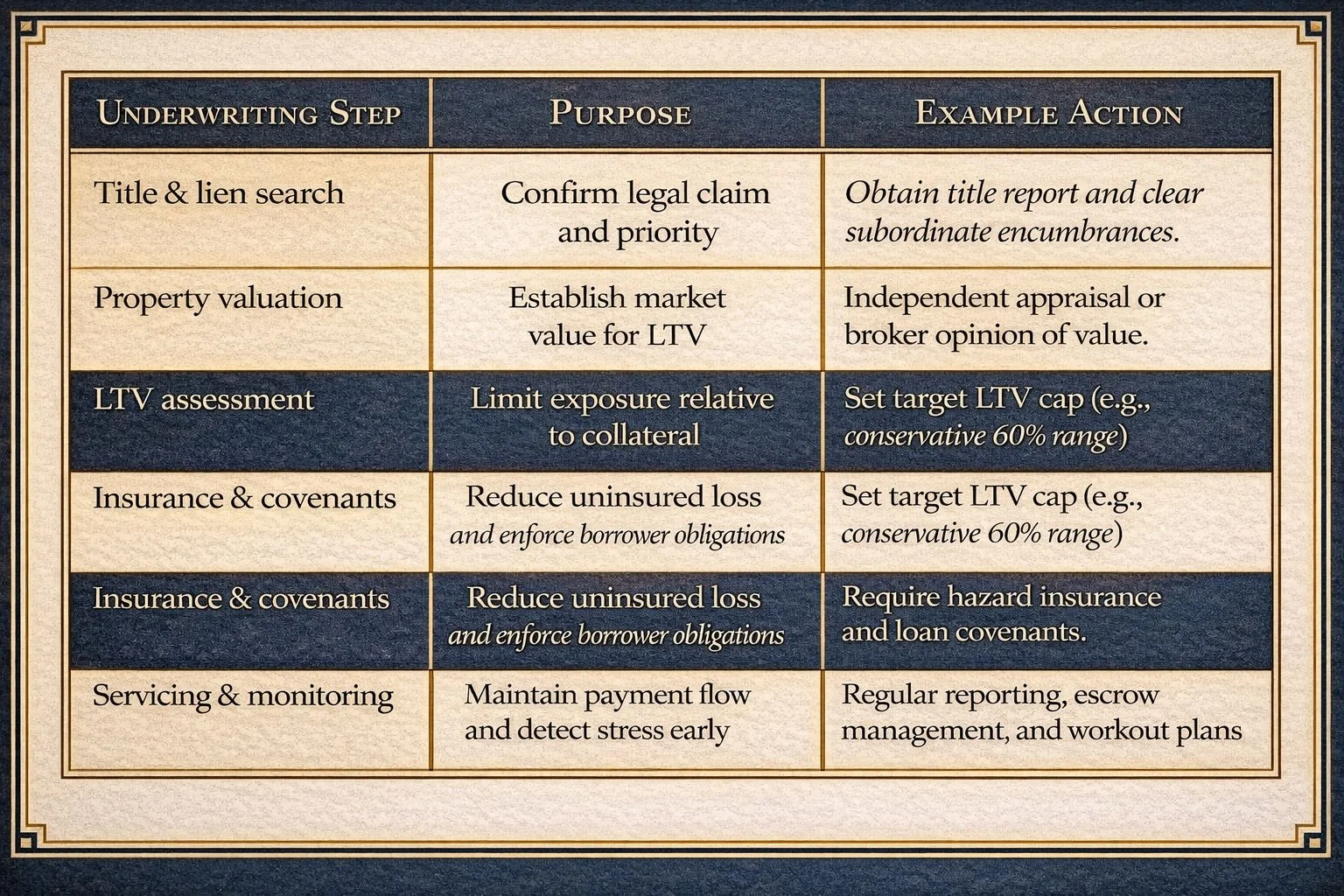

Blue Bay Fund I follows a stepwise underwriting framework combining title verification, property‑based valuation, conservative LTV limits, and ongoing monitoring to preserve capital and manage performance risk. The fund targets secured liens to real estate investment projects, enforces prudent LTV thresholds, and requires title searches and hazard insurance for recoverability. Active servicing and periodic valuation reviews are integral lifecycle controls, with investments selected for predictable cash flow and collateral quality.

The fund’s underwriting framework relies on repeatable controls to improve recovery odds and support stable income.

What Are the Current Market Trends and Outlook for Real Estate Private Credit in 2026?

The private credit market will enter 2026 with continued expansion, driven by rising institutional allocations and yield‑seeking behavior, even as traditional lenders pull back from specific real estate segments. Key drivers include tighter bank regulation, investor demand for income in a higher‑rate environment, and broader private market access for accredited investors. Forecasts point to ongoing growth in private credit assets under management, supported by steady sponsor demand and a structural tilt toward direct lending, underpinning a constructive near‑term outlook for secured real estate debt strategies. Interest rates and regulatory policy shape loan pricing, borrower behavior, and fund return profiles.

How Can Accredited Investors Access and Invest in Real Estate‑Secured Private Credit?

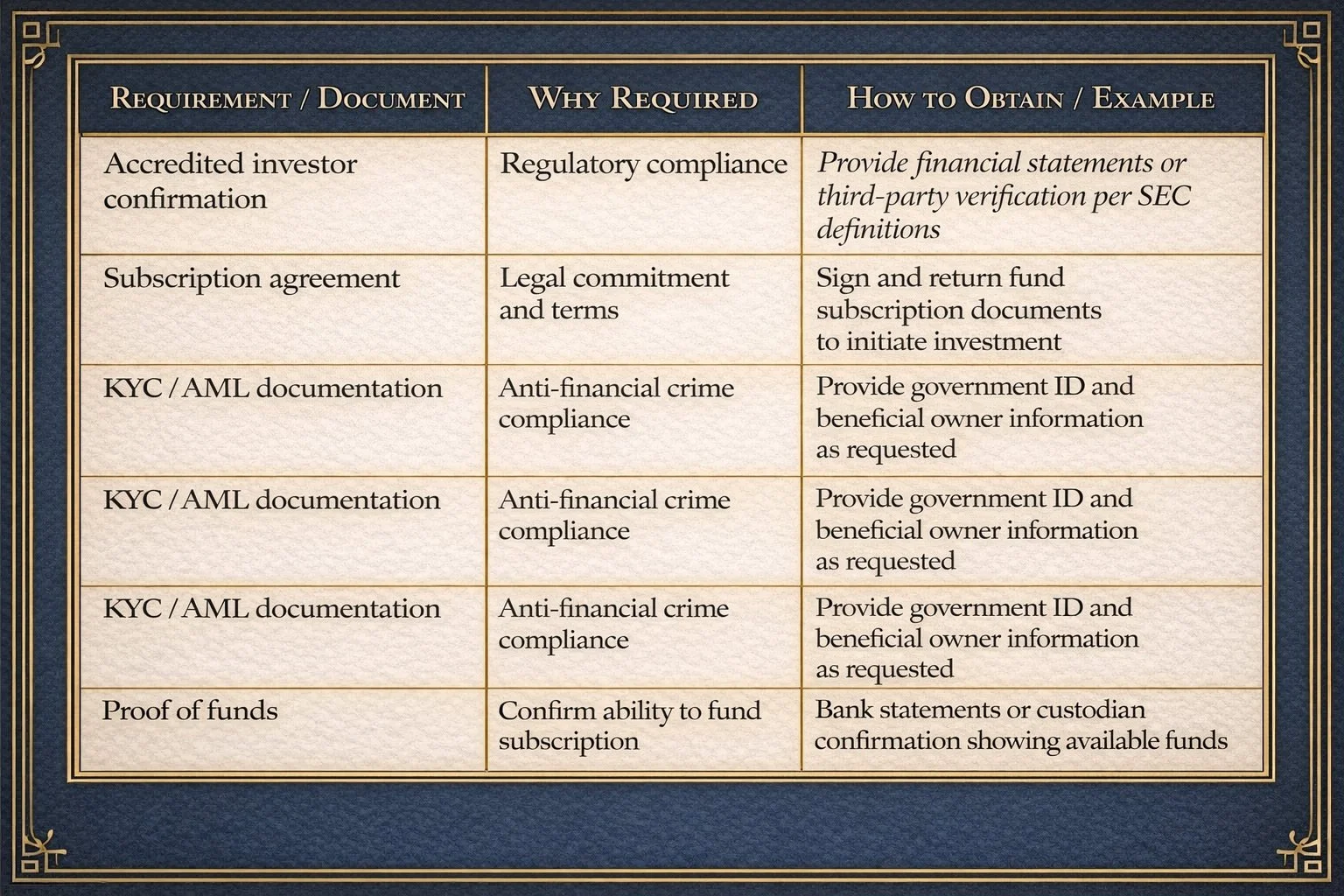

Accredited investors access real estate‑secured private credit via direct funds, pooled vehicles, or by purchasing individual mortgage notes. Direct funds and pooled vehicles require onboarding processes, which typically include investor qualification, subscription documentation, funding, and periodic reporting. The process prioritizes regulatory compliance—verifying accredited status—followed by subscription execution and funding. Investors should expect limited liquidity and hold periods consistent with private credit structures, along with regular reporting and distributions. Blue Bay Fund I follows standard SEC accredited investor criteria, requiring verification of income or net worth thresholds.

Typical verification steps influence eligibility and documentation for fund access.

The investor process follows a clear sequence:

Inquiry: Request offering materials and initial information.

Qualification: Provide accredited investor verification documents.

Subscription: Review and sign subscription agreements.

Funding: Transfer subscription funds per instructions.

Reporting: Receive periodic performance and distribution statements.

These steps outline the practical path from interest to active investment and set expectations for timing and documentation.

How Does Values‑Driven Investing Connect with Real Estate Private Credit?

Values‑driven investing aligns capital allocation with stewardship principles, faith‑based legacy goals, and disciplined decision‑making, prioritizing capital preservation and intergenerational transfer. Choosing secured, first‑position real estate debt allows investors to pursue returns supporting predictable income for family stewardship and philanthropic intent, pairing financial goals with faith‑aligned priorities. Faith‑informed stewardship centers on preserving capital across generations, making conservative, collateral‑backed investments a natural fit.

Frequently Asked Questions About Real Estate Notes

What are high-yield real estate notes?

High-yield real estate notes are mortgage loans secured by property. Investors earn interest income, typically at higher rates than traditional fixed-income. They offer passive income without property management, often backed by a first-lien mortgage for security and stable returns.

How do I assess the risks associated with high-yield real estate notes?

Assess risks by evaluating underlying real estate, the borrower's credit profile, and market conditions. Conduct thorough due diligence, including appraisals and financial assessments. Understanding note terms, interest rates, and repayment schedules is crucial. Diversifying investments also mitigates risks.

Can I invest in high-yield real estate notes if I am not an accredited investor?

Typically, high-yield real estate notes are offered to accredited investors, who meet specific income or net worth criteria. Some platforms may offer opportunities for non-accredited investors through different investment vehicles. Research requirements and regulations, and consult a financial advisor for suitable options.

What is the typical return on investment for high-yield real estate notes?

Returns vary based on note terms, risk profile, and market conditions. Investors generally expect 8-15% annually, depending on risk and duration. Compare these returns with other options and consider associated risks.

How does the Blue Bay Fund I ensure transparency for real estate investors?

Blue Bay Fund I ensures transparency through open reporting and clear communication. This includes detailed information on investment performance, fees, and underlying assets. Regular updates keep investors informed, fostering trust and accountability.

What should I consider before transitioning from a landlord to a real estate lender?

Consider your financial goals, risk tolerance, and desired involvement. Evaluate passive income from real estate notes (private mortgage investments) versus active rental property management. Assess market conditions, note types, and conduct due diligence for a successful transition.

How can I get started with investing in high-yield real estate notes?

Educate yourself on the market and note types. Research reputable platforms or funds, like Blue Bay Fund I. Meet accreditation requirements if applicable. Consult a financial advisor for a tailored investment strategy.

Conclusion

Real estate‑secured private credit offers accredited investors a practical path to stability, predictable income, and capital preservation through collateral‑backed lending. Understanding secured lending mechanics and conservative underwriting allows investors to align financial objectives with values‑based stewardship and legacy planning. With private credit markets expanding, now is an opportune time to evaluate these opportunities. Review our offering materials and investor resources to support your long‑term financial goals.

Edwin D. Epperson III,

Manager & CEO

Soli Deo Gloria