Christian Investing: Faithful Stewardship in Retirement

You spent decades building something. Now the question isn't how to make more — it's how to protect what you have, generate income you can count on, and stay free to give. For many of us, that's not just financial planning. That's a calling.

Christian investing gets talked about a lot. Stock screens, ESG funds, impact portfolios. But for most people of faith who've reached retirement, the real question is simpler: Am I being a faithful steward of what God entrusted to me? That question deserves a serious answer. Not a product pitch.

Want to see exactly how your principal is protected before committing a dollar? That's what the overview is for.

GET THE OVERVIEW →The Parable of the Talents: It's About Who You Trust, Not What You Do

In Matthew 25, a master entrusts his servants with capital before a long journey. Two put it to work and multiply it. One buries his in the ground to "keep it safe." When the master returns, he praises the first two — and rebukes the third. But notice why the third servant buried it: he said, "I was afraid." He had a wrong view of his master — hard, demanding, unpredictable. His paralysis wasn't laziness. It was a failure of trust.

The faithful servants didn't act because productivity is virtuous. They acted because they knew their master's character — and that knowledge freed them to steward wisely. That's the Reformed heart of this passage: right action flows from right understanding of who God is. Faithful stewardship isn't self-generated discipline. It's the fruit of trusting a good and sovereign God with what He's already given you.

"You should have put my money on deposit with the bankers, so that when I returned I would have received it back with interest."

— Matthew 25:27

What Stewardship Looks Like After You've Sold the Business

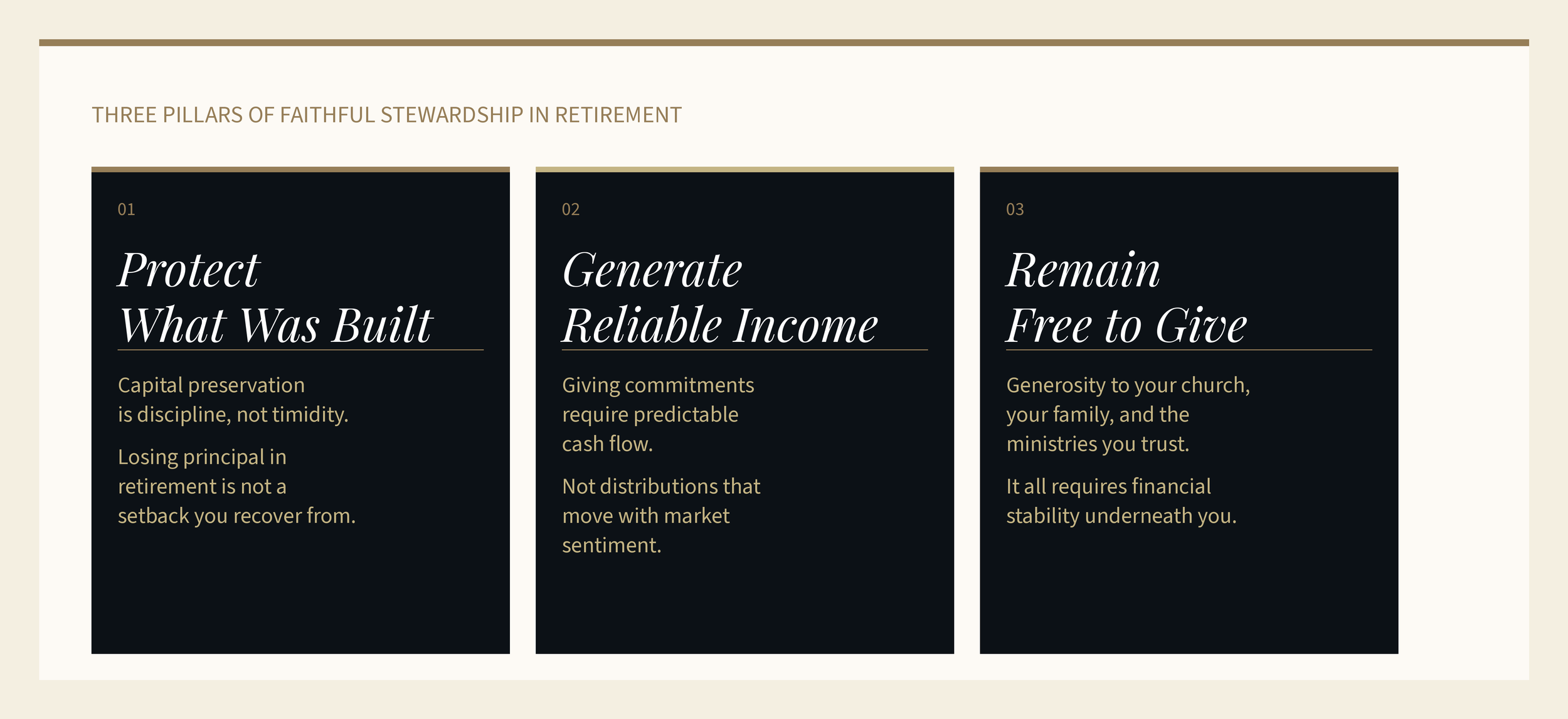

Most investing conversations are built around growth. That framework makes sense at 40. It makes far less sense when your income needs to be predictable, your principal is irreplaceable, and you have giving commitments you intend to honor. For a Christian in retirement, faithful stewardship looks like three things:

Why the Stock Market Feels Wrong and That Instinct May Be Sound

Many people of faith feel an unease about the market they can't quite name. Owning a fraction of a company you've never visited, whose value can evaporate overnight based on someone else's fear. It doesn't feel grounded. That instinct isn't naive. It may be pointing you toward real assets. Real collateral. Something you can understand and explain to your children.

Many retirees have tried rental property. The math made sense: buy, collect rent, build equity. But then came the tenants who don't pay, the roof that fails at the worst time, and the 11 p.m. emergency call. It's a second job. In retirement, you've already done the work

Being the Bank: A Better Way to Own Real Estate

What if instead of owning the property, you were the lender? Your capital is secured by a first-lien mortgage on real property, without ever becoming a landlord. That's private mortgage lending, and it's one of the oldest financial instruments in existence

How Blue Bay Fund Works — Simply

You

Accredited

Investor

Blue Bay Fund

Originates &

underwrites

mortgage loans

Borrower

Secured by

real property

Monthly Income

Paid to you.

First-lien secured.

Sub-70% LTV.

Your principal is protected by the property — not market performance

First-lien position means you're first in line if something goes wrong. Before anyone else gets paid, you do. Conservative loan-to-value (LTV) means the loan is only a portion of the property's value, typically under 70%, so significant equity cushions your principal even if values fall. No market timing. No earnings surprises. You're lending against real property, earning interest, and getting paid monthly. Simple. Secure. Understandable.

Want to see exactly how your principal is protected before committing a dollar? That's what the overview is for.

GET THE OVERVIEW →Does Your Portfolio Reflect Who You Are?

If you've built a life around integrity, family, generosity, and faith, it's worth asking whether your investments reflect that. Is your capital doing something real, something you can stand behind, something that doesn't require you to look away?

For many people of faith approaching or living in retirement, the answer to that question points toward real assets, honest structures, and predictable income. That's not a restriction. It's a clarification. And it makes the decision simpler.

Faith-Based Investing: Aligning Your Capital With Your Convictions

Faith-based investing is not just about avoiding companies that conflict with your values. It is about making intentional, biblically responsible investing decisions that reflect who you are and what you believe. For many Christians, that means moving away from mutual funds and complex financial products and services they cannot fully understand or stand behind, and toward investment strategies grounded in real assets and honest structures.

The goal is not to avoid investing altogether. It is to invest in a way that is aligned with biblical principles, supports your giving, and reflects the integrity you have built your life around.

That is not a limitation. That is clarity.

This article is for educational purposes only and does not constitute investment advice. Private fund investments involve risk, including possible loss of principal. Blue Bay Fund I is available only to accredited investors. Please review all offering documents carefully before investing.

With Honor,

Edwin D. Epperson III,

Manager & CEO

Soli Deo Gloria